- The Strategic Tax Advisor

- Posts

- Breaking Down the Walls: How New Policy Changes Could Transform Your 401(k) Investment Options

Breaking Down the Walls: How New Policy Changes Could Transform Your 401(k) Investment Options

Prashanth Srikanthan

August 24, 2025

Picture this scenario: You're sitting in your company's break room, staring at a 401(k) enrollment form. The financial advisor at the front of the room has just finished explaining your "exciting" investment options using terms like "conservative," "moderate," and "aggressive" risk levels. You check a box, submit the form, and walk away wondering if there might be better ways to grow your retirement savings. For millions of Americans, this experience represents the extent of their retirement investment decision-making power.

In August 2025, this limited landscape began its transformation with the signing of the "Executive Order on Democratizing Access to Alternative Assets for 401(k) Investors." This policy initiative aims to expand investment options within employer-sponsored 401(k) plans, potentially giving workers access to the same types of alternative investments that wealthy individuals and institutions have used for decades to build wealth. To understand why this matters so much, we need to first examine how the current system has essentially created two different investment worlds – one for ordinary Americans and another for the wealthy.

Understanding the Current 401(k) Limitation Problem

Before diving into what might change, let's examine why your current 401(k) options feel so restrictive. The traditional 401(k) system operates within what we might call the "Wall Street Box" – a carefully controlled environment where your investment choices are typically limited to stock mutual funds, bond mutual funds, target-date funds, exchange-traded funds (ETFs), and money market accounts.

These options represent what financial institutions consider "safe" and easily manageable investments for the masses. However, this safety-first approach has created an interesting paradox. While university endowments, pension funds, and high-net-worth individuals routinely allocate significant portions of their portfolios to alternative assets and achieve superior returns, average Americans are essentially told these same strategies are "too risky" or "too complex" for their retirement accounts.

Consider the numbers that illustrate this disparity. Americans have approximately $8 trillion invested in 401(k) plans, representing the primary retirement savings vehicle for millions of workers. Yet these massive pools of capital are restricted to a narrow band of investment options, while sophisticated investors with access to alternatives often outperform traditional portfolios over long time horizons.

What Alternative Assets Actually Mean

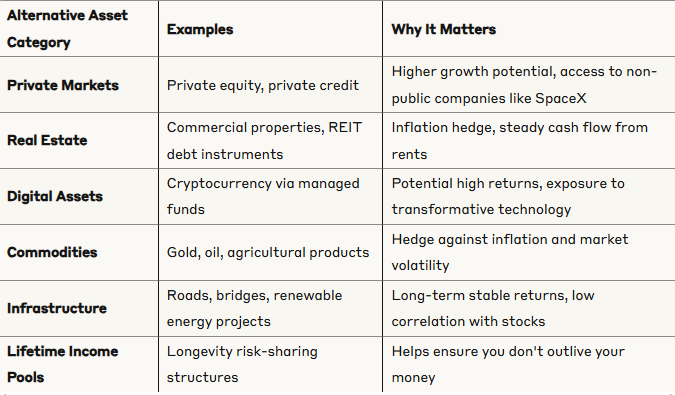

The term "alternative assets" might sound exotic or complicated, but many of these investments are actually quite familiar once you understand them. The executive order specifically identifies several categories of alternative investments that could become available in 401(k) plans.

Alternative Asset Categories Available Through the New Executive Orde

Let's break down why each of these matters for your retirement security.

Private markets represent one of the most significant opportunities because they provide access to companies that don't trade on public stock exchanges. Think about this for a moment: many of today's most successful companies, from SpaceX to various renewable energy projects, remain private for much longer than companies did in previous decades. Private equity funds can take longer-term approaches to building value because they don't worry about quarterly earnings pressure that affects public companies.

Real estate investments extend far beyond simply buying a rental property. In the 401(k) context, these investments might include commercial real estate projects or development projects for infrastructure like apartment complexes. Real estate serves a crucial role because it typically provides both regular income through rents and long-term appreciation, while often acting as an inflation hedge – when prices rise throughout the economy, real estate values and rents typically rise as well.

Digital assets represent the modern frontier of alternative investing, primarily focused on cryptocurrency exposure through professionally managed funds. Rather than individual investors trying to navigate cryptocurrency exchanges directly, 401(k) participants would likely access these through managed funds that handle the technical complexities and security concerns.

Commodities encompass physical goods that form the foundation of economic activity – gold, oil, agricultural products, and industrial metals. These investments often perform well during inflationary periods or economic uncertainty, providing a hedge against both market volatility and currency devaluation. When stock and bond markets struggle, commodities often maintain or increase their value because people and businesses still need these fundamental resources regardless of financial market conditions.

Infrastructure investments involve funding the essential systems that keep our economy running: roads, bridges, power plants, telecommunications networks, and renewable energy projects. These investments typically provide steady, predictable cash flows over long periods because people and businesses consistently need these services regardless of economic conditions. Infrastructure investments also tend to have low correlation with stock market performance, meaning they can provide stability when other investments are volatile.

Lifetime income pools represent an innovative approach to one of retirement planning's biggest challenges: the risk that you'll outlive your money. These risk-sharing structures pool longevity risk across many participants, helping ensure that retirees receive income throughout their lifetimes even if they live longer than average life expectancy projections. This addresses a critical gap in traditional retirement planning that assumes fixed withdrawal rates over predetermined time periods.

The Regulatory Machinery: How Government Agencies Are Making This Happen

Understanding how this transformation will unfold requires examining the specific regulatory mechanisms that government agencies will use to implement these changes. The executive order doesn't simply declare that 401(k) plans can now include alternatives – it sets in motion a carefully orchestrated process involving multiple agencies with different roles and timelines.

The Department of Labor has already taken immediate action by rescinding previous guidance from 2021 that had discouraged 401(k) plan fiduciaries from including alternative assets in their investment lineups. This 2021 statement had created a chilling effect throughout the industry, essentially warning plan sponsors that including alternatives could expose them to regulatory scrutiny and potential legal liability. By removing this discouragement, the DOL has already begun clearing the path for alternatives.

However, removing obstacles represents only the first step. The more complex challenge involves providing clear, actionable guidance that helps plan fiduciaries understand exactly how they can prudently include alternative assets without exposing themselves to legal risk. The DOL has been given until February 2026 to develop detailed guidance that will essentially create a roadmap for including alternatives in 401(k) plans. This guidance will need to address crucial practical questions about how plan fiduciaries should evaluate fees, what liquidity requirements should apply, and how plans should handle valuation challenges.

The Securities and Exchange Commission plays a complementary role focused on reviewing investor qualification rules that currently limit access to many alternative investments. By facilitating broader access to these investments, the SEC could make it easier for 401(k) platforms to include alternatives that were previously restricted to wealthy investors.

Timeline and Implementation Reality: What You'll Actually Experience

Understanding when and how these changes will appear in your 401(k) plan requires recognizing that the transformation will be largely invisible to most participants initially. Rather than seeing dramatic new investment menus with options labeled "Buy Real Estate Fund" or "Cryptocurrency Investment," most people will experience these changes through gradual evolution of their existing investment options.

The implementation will primarily happen through three existing structures that most 401(k) participants already use without thinking much about them.

Target-Date Funds: The most common way you'll gain alternative asset exposure without even noticing. If you're currently invested in a 2050 Target Date Fund, it might gradually shift from 0% alternatives to 10% alternatives (private equity, real estate, infrastructure) while reducing traditional allocations slightly. This gives you access to investments once reserved exclusively for pension funds and university endowments.

How Target-Date Fund Allocations May Evolve (Example: 2055 Target Date Fund)

Collective Investment Trusts (CITs): Another invisible pathway used in large 401(k) plans that offer lower costs than retail mutual funds. As CITs begin incorporating alternative asset components, you benefit from professional alternative asset management without needing to understand the underlying complexity or make any investment decisions yourself.

The timeline for experiencing these changes will vary significantly based on your employer and 401(k) provider. Technology companies and financial services firms may begin offering alternative asset exposure within 12-18 months of final regulatory guidance being issued in February 2026. Larger companies with more resources will likely follow within 2-3 years, while smaller employers and more conservative industries may take 3-5 years to fully embrace alternative asset options.

Understanding the Benefits: Why This Transformation Matters for Your Future

To truly appreciate why this policy change could be significant for your retirement security, we need to examine the concrete benefits that alternative assets can provide and why they've been so successful for institutional investors like pension funds and university endowments.

Diversification represents the most fundamental benefit, but it's important to understand what true diversification actually means beyond the typical "don't put all your eggs in one basket" explanation. Traditional 401(k) portfolios, even those that include both stocks and bonds from different countries, still suffer from a crucial limitation: they're entirely dependent on public markets. When economic stress affects public markets, it tends to affect all public market investments simultaneously, regardless of whether they're U.S. stocks, international stocks, or government bonds.

Alternative assets provide diversification precisely because they don't depend entirely on public market sentiment and behavior. Real estate values are driven by factors like population growth and local economic conditions that don't necessarily correlate with stock market movements. Private equity investments can take longer-term approaches to building value. Infrastructure investments generate cash flows from essential services that people need regardless of stock market performance.

Access to institutional-quality investment strategies represents another crucial benefit that's often underappreciated. For decades, pension funds, university endowments, and wealthy individuals have allocated significant portions of their portfolios to alternative assets, often achieving better long-term returns than traditional stock and bond portfolios. The Yale Endowment, for example, has famously allocated more than half of its portfolio to alternative assets and achieved superior returns over multiple decades.

Inflation protection becomes increasingly important as we consider longer lifespans and the challenge of maintaining purchasing power over retirement periods that might last 30 years or more. Traditional bond investments actually lose purchasing power during inflationary periods because their fixed interest payments become worth less as prices rise. Real estate and commodities, by contrast, often perform well during inflationary periods because their values tend to rise along with general price levels.

Understanding the Risks: What You Need to Consider Carefully

While the potential benefits of alternative assets are compelling, developing a complete understanding requires examining the genuine challenges and risks that come with these investments. These risks aren't necessarily reasons to avoid alternatives, but they are important factors to understand before embracing them as part of your retirement strategy.

Higher fees represent perhaps the most immediate and tangible challenge you'll encounter with alternative assets. Traditional index funds often charge fees of less than 0.1% annually, meaning you pay less than $1 per year for every $1,000 invested. Alternative asset funds operate very differently, with fee structures that often include both management fees and performance fees. Management fees for private equity funds might range from 1% to 2% annually, while performance fees might claim 15% to 20% of investment profits above certain thresholds.

To understand why these fees matter for your long-term wealth building, consider a simple example. If you invest $10,000 in a low-cost index fund charging 0.05% annually, you'll pay $5 per year in fees. If that same $10,000 goes into an alternative asset fund charging 1.5% annually, you'll pay $150 per year in fees – thirty times more. Over several decades of investing, these fee differences compound significantly and can substantially impact your final retirement balance.

Liquidity challenges create another dimension of complexity that's particularly important in retirement accounts. When you own stocks or bonds through mutual funds, you can typically sell your shares and access your money within a few business days. Alternative assets often work very differently, with some investments requiring you to commit your money for multiple years without the ability to withdraw it easily.

Valuation challenges present ongoing complexity that most traditional investors haven't encountered before. When you own shares of Apple stock, you can check their exact value any time during market hours because millions of shares trade daily. Alternative assets don't have this transparent pricing mechanism. How do you determine the exact value of a private equity fund's stake in a company that doesn't trade publicly?

Current Opportunities vs. Future Possibilities: Understanding What's Available Today

While we anticipate significant changes to 401(k) investment options over the coming years, understanding your current alternatives helps put these future developments in proper context. Individual Retirement Accounts currently provide remarkably broad investment flexibility that most people never fully utilize. The IRA market actually contains more total assets than 401(k) plans – approximately $17 trillion compared to $8 trillion in workplace retirement accounts.

Investment Access Comparison Across Retirement Account Types

This comparison reveals a significant opportunity gap where millions of Americans could be accessing alternative investments immediately through IRA rollovers rather than waiting for policy changes to filter through their employer's retirement plan.

The rollover opportunity represents one of the most immediate and powerful ways to access alternative investments today. Many people have old 401(k) accounts from previous employers sitting dormant with limited investment options and potentially high fees. These accounts can typically be rolled over into self-directed IRAs that unlock the full spectrum of alternative investment possibilities. If you're interested in exploring how to use IRAs for alternative investments, feel free to contact me - as a tax advisor specializing in self-directed retirement accounts, I can help you navigate the opportunities and requirements.

Taking Action in Your Retirement Planning Today

The transformation of 401(k) investment options represents an important development in retirement planning, but the most crucial insight from this analysis is recognizing that you don't need to wait passively for these changes to improve your retirement investment strategy.

Begin by conducting a comprehensive audit of your existing retirement accounts, paying particular attention to any old 401(k) accounts from previous employers that might be sitting dormant. These forgotten accounts often contain significant balances that could be rolled over into self-directed IRAs, immediately unlocking alternative investment possibilities.

When evaluating your current 401(k) participation, consider adjusting your strategy to account for future alternative asset availability. If you're currently contributing enough to receive your full employer match, you might maintain that contribution level while directing additional retirement savings toward IRAs that offer immediate alternative asset access.

Research and education represent crucial next steps for anyone interested in alternative investing, because these asset classes require more knowledge and due diligence than traditional mutual fund investing. Start by focusing on one alternative asset class that particularly interests you or aligns with your professional knowledge. The learning process should be gradual and systematic rather than rushed.

Start with modest allocations that won't create financial stress if they don't perform as expected. Many successful alternative investors begin by allocating 5% to 10% of their retirement assets to alternatives while they build knowledge and experience. This approach allows you to learn how these investments behave in your portfolio while you develop expertise.

The Bigger Picture: Understanding This Transformation in Context

The push for expanded 401(k) investment options reflects broader changes in American retirement planning that extend far beyond investment menu choices. Traditional pension plans, which provided guaranteed retirement income for previous generations, have largely disappeared from the private sector. Social Security provides only a basic foundation of retirement income that most people need to supplement substantially.

This shift toward individual responsibility for retirement security creates both challenges and opportunities. The challenge lies in requiring ordinary Americans to make sophisticated investment decisions that affect their financial security for decades. The opportunity lies in providing access to investment strategies that were previously available only to institutions and wealthy individuals, potentially improving retirement outcomes for people who take advantage of these expanded options.

Understanding this context helps inform your strategic approach to retirement planning. Rather than depending entirely on policy continuity, building investment knowledge and experience that works regardless of regulatory changes creates more robust long-term financial security. The skills and knowledge you develop through alternative investing in IRAs will serve you well regardless of whether 401(k) alternative access expands, contracts, or remains unchanged over time.

Moving Forward with Confidence and Wisdom

The democratization of alternative asset access represents a significant positive development for American retirement savers, but success with these expanded options requires approaching them with appropriate knowledge, caution, and realistic expectations. Alternative investments aren't magic solutions that automatically produce better returns than traditional investments, but they do provide additional tools for building diversified, resilient retirement portfolios.

The key to successful alternative investing lies in understanding that it represents a long-term learning and relationship-building process rather than a simple asset allocation decision. For most people, the immediate opportunity lies not in waiting for 401(k) policy changes, but in beginning to explore alternative investments through existing IRA options while these policy changes unfold.

Remember that retirement investing success ultimately depends more on consistent saving, appropriate diversification, reasonable risk management, and long-term perspective than on access to any particular type of investment. Alternative assets can enhance a well-designed retirement portfolio, but they work best as part of a comprehensive strategy rather than as the entire foundation of your retirement security.

Disclaimer

This blog post is provided for educational and informational purposes only and should not be construed as investment advice, financial advice, or recommendations for specific investment products or strategies. The information presented does not constitute an attorney-client or financial advisor-client relationship.

Investment in alternative assets involves significant risks, including the potential for total loss of invested capital, lack of liquidity, and complex tax implications. Alternative investments may not be suitable for all investors and should only be considered as part of a well-diversified investment portfolio after careful consideration of your individual financial situation, risk tolerance, and investment objectives.

Before making any investment decisions, you should consult with qualified legal, tax, and financial professionals who can provide advice based on your specific circumstances. Past performance of any investment does not guarantee future results. All investments carry risk, and you may lose some or all of your investment.

The regulatory and policy landscape surrounding retirement accounts and alternative investments is subject to change. Current laws, regulations, and policies may be modified or reversed by future administrations or regulatory actions. You should stay informed about regulatory changes that may affect your investment options and strategies.

This content is based on information available at the time of writing and may not reflect the most current developments in relevant laws, regulations, or market conditions. Always verify information with current, authoritative sources before making financial decisions.