- The Strategic Tax Advisor

- Posts

- Debunking the 'Lower Tax Bracket in Retirement' Myth That's Costing You Hundreds of Thousands

Debunking the 'Lower Tax Bracket in Retirement' Myth That's Costing You Hundreds of Thousands

Understanding the true lifetime tax cost of traditional retirement savings

Prashanth Srikanthan

September 08, 2025

Picture this scenario: You diligently save for retirement, maximize your 401(k) contributions, and feel great about the tax deductions you receive each year. Fast forward thirty years, and you discover that every dollar you "saved" in taxes actually cost you six dollars in retirement. Sound impossible? Let me walk you through the mathematics that reveal one of the most misunderstood aspects of retirement planning.

The Foundation: Understanding Tax-Deferred vs. Tax-Free Growth

Before we dive into the numbers, let's establish the fundamental difference between traditional and Roth retirement accounts. Think of it like this: the government offers you two payment plans for your retirement taxes.

Option A (Traditional 401k/IRA): Pay taxes later on everything you withdraw, including all the growth your money earned over the decades.

Option B (Roth 401k/IRA): Pay taxes now only on what you contribute, then never pay taxes again on that money or its growth.

Most people instinctively choose Option A because they see an immediate tax break. But this decision requires us to make a critical assumption: that we'll pay less in total taxes during retirement than we save during our working years.

Meet Alex: A Case Study in Retirement Tax Planning

Let's examine this assumption through the lens of a real example. Alex represents many professionals today - someone who earns a solid living and diligently saves for retirement. Here are Alex's details:

Annual income: $160,000

Current marginal tax bracket: 24%

Annual 401(k) contribution: $18,000

Expected investment return: 7% annually

Years until retirement: 25

Expected years in retirement: 25

Alex chooses traditional 401(k) contributions because the immediate tax savings feel tangible and beneficial.

Phase One: The Accumulation Years (The Visible Savings)

During Alex's working years, the math appears straightforward and favorable. Each year, Alex contributes $18,000 to the traditional 401(k), which reduces taxable income from $160,000 to $142,000.

Annual Tax Savings Calculation:

Contribution amount: $18,000

Marginal tax rate: 24%

Annual tax savings: $18,000 × 24% = $4,320

25-Year Tax Savings Summary:

Total contributions: $450,000

Total tax savings: $108,000

Account value at retirement (7% growth): $1,822,470

This seems like an excellent deal. Alex has saved $108,000 in taxes over 25 years while building a substantial retirement nest egg.

Phase Two: The Distribution Years (The Hidden Costs)

Now comes the critical part that most people underestimate. When Alex begins retirement, every dollar withdrawn from that traditional 401(k) becomes taxable income at ordinary income tax rates.

Let's assume Alex follows the commonly recommended 4% withdrawal rule, adjusted annually for inflation at 2.5%.

Year-by-Year Withdrawal Analysis

How Alex's retirement withdrawals create an escalating tax burden over 25 years. Notice how the effective tax rate increases from 12% to over 20% as withdrawal amounts grow with inflation adjustments.

Total taxes paid on retirement distributions over 25 years: $475,230

Already, we can see that Alex will pay more than four times more in taxes during retirement ($475,230) than was saved during the working years ($108,000). But this is only the beginning of the story.

Here's where the retirement tax calculation becomes particularly complex and expensive. Social Security benefits can become taxable based on what the IRS calls "combined income" or "provisional income."

Provisional Income Formula: Adjusted Gross Income + Non-taxable Interest + 50% of Social Security Benefits

For someone receiving Alex's projected Social Security benefit of $36,000 annually, let's see how the traditional 401(k) withdrawals affect the taxation of those benefits.

The income levels that trigger Social Security benefit taxation. Key insight: These thresholds haven't been adjusted for inflation since 1993, making them easier to exceed than most people realize.

Let's assume Alex is single for this analysis. In the first year of retirement, Alex's combined income calculation looks like this:

Traditional 401(k) withdrawal: $72,899

50% of Social Security: $18,000

Combined income: $90,899

Since this far exceeds $34,000, up to 85% of Alex's Social Security becomes taxable.

The Compounding Effect Over Time

How Alex's growing 401(k) withdrawals create an escalating Social Security tax burden. The "Additional Tax" column shows the yearly cost of having retirement account withdrawals push Social Security benefits into taxable territory.

Total additional taxes on Social Security over 25 years: $147,890

The final layer of hidden costs comes through Medicare's Income-Related Monthly Adjustment Amount (IRMAA). This is perhaps the most misunderstood "tax" in retirement because it doesn't feel like a tax - it appears as a higher insurance premium. But make no mistake: IRMAA functions as an additional income tax on retirement withdrawals.

What Exactly is IRMAA?

IRMAA stands for "Income-Related Monthly Adjustment Amount." When your income exceeds certain thresholds, Medicare requires you to pay higher premiums for both Part B (medical insurance) and Part D (prescription drug coverage). These surcharges are calculated based on your income from two years prior.

Why This Matters for 401(k) Withdrawals:

Your traditional 401(k) withdrawals count as ordinary income

Higher withdrawals = higher reported income

Higher income = higher Medicare premiums

These premium increases continue for as long as your income stays elevated

How Medicare premiums increase with income levels. These surcharges function as additional taxes on retirement income because they're based on your Modified Adjusted Gross Income (MAGI), which includes traditional 401(k) withdrawals.

Medicare Part D prescription drug premium surcharges that accompany the Part B surcharges. Together, these create a combined "stealth tax" on retirement income that many people don't anticipate.

Detailed Medicare IRMAA Impact Analysis for Alex

Let's trace how Alex's growing withdrawal amounts trigger Medicare premium surcharges over time:

When Alex's retirement withdrawals trigger Medicare premium surcharges and the combined cost of both Part B and Part D penalties. The "Total Extra" column shows how these surcharges compound over time as withdrawal amounts increase.

📊 Complete IRMAA Impact Breakdown

💰 Combined Part B + Part D Surcharges

🟢 Standard Rate (Income under $103,000)

└── Part B: $2,096 | Part D: $0 surcharge | Total extra: $0

🟡 Tier 1 Surcharge (Income $103,001-$129,000)

└── Part B: $2,935 (+$839) | Part D: +$155 | Total extra: $994

🔴 Tier 2 Surcharge (Income $129,001-$161,000)

└── Part B: $4,193 (+$2,097) | Part D: +$400 | Total extra: $2,497

📈 25-Year Complete Cost Timeline

🗓️ Years 1-10: Standard Rate

▪️ Extra Medicare costs: $0

🗓️ Years 11-20: Tier 1 Surcharge

▪️ $994 × 10 years = $9,940

🗓️ Years 21-25: Tier 2 Surcharge

▪️ $2,497 × 5 years = $12,485

🎯 Total Additional Medicare Costs: $22,425

Why IRMAA is Particularly Devastating

The "Two-Year Lag" Problem: Medicare uses your income from two years ago to set this year's premiums. This means:

You can't easily adjust mid-year to reduce premiums

Large withdrawal years (like Roth conversions) impact you for multiple years

Planning becomes much more complex

The "Cliff Effect" Problem: IRMAA brackets create sharp jumps in costs. Earning $129,000 vs $129,001 costs an extra $1,458 annually ($2,097 vs $639 in surcharges). A single dollar of income can trigger hundreds in additional premiums.

The "Compounding" Problem: Unlike regular income taxes that you pay once, IRMAA surcharges continue every month for as long as your income stays elevated. Traditional 401(k) withdrawals essentially guarantee elevated income throughout retirement.

Note: IRMAA brackets and amounts are updated annually and subject to change. These calculations use 2024 figures and should be verified with current Medicare guidance.

The Complete Financial Picture

Now let's step back and examine the full lifetime tax impact of Alex's traditional 401(k) strategy:

The complete lifetime tax impact of Alex's traditional 401(k) strategy. This summary shows how the $108,000 in working-years tax savings ultimately results in $675,560 in total retirement taxes and penalties - a 6.3-to-1 negative return on the original "tax savings."

Alex saved $108,000 in taxes to ultimately pay $675,560 in retirement-related taxes and penalties - 6.3 times more than the original tax savings.

Understanding the Roth Alternative

Let's examine what would have happened if Alex had chosen Roth 401(k) contributions instead.

The Roth Scenario

With Roth contributions, Alex would have paid the $108,000 in taxes upfront during the working years. However, this creates several significant advantages:

No taxes on distributions: All withdrawals from the Roth account are tax-free

No impact on Social Security taxation: Roth withdrawals don't count toward provisional income

No Medicare premium surcharges: Roth distributions don't affect IRMAA calculations

No required minimum distributions: Unlike traditional accounts, Roth IRAs don't force withdrawals at age 73

The Tax-Free Retirement Income Stream

Instead of paying $675,560 in taxes and penalties over retirement, Alex would pay zero additional taxes beyond the initial $108,000 paid during the working years.

Net tax savings with Roth strategy: $567,560

Beyond Traditional and Roth: Whole Life Insurance as a Tax-Advantaged Retirement Vehicle

Beyond traditional 401(k)s and Roth accounts lies a lesser-known but powerful retirement income strategy: properly structured whole life insurance. While most people think of life insurance purely as protection, certain types of permanent life insurance can serve as sophisticated tax-advantaged retirement savings vehicles.

Understanding Whole Life Insurance Mechanics

Think of whole life insurance as having two components working together: a death benefit (the insurance protection) and a cash value account (the savings component). The cash value grows over time through premium payments and dividends from the insurance company, creating a pool of money you can access during your lifetime.

Here's what makes this strategy unique from a tax perspective:

Tax-Advantaged Growth: The cash value grows without current taxation, similar to funds inside a 401(k) or IRA.

Tax-Free Access: You can access this cash value through policy loans and partial withdrawals without creating taxable income, similar to Roth distributions but with different mechanics.

No Required Distributions: Unlike traditional retirement accounts, there are no mandatory withdrawals at age 73.

Death Benefit Protection: If structured properly, your beneficiaries receive the remaining death benefit income-tax-free.

How Alex Could Integrate Whole Life Insurance

Let's examine how Alex might incorporate a whole life insurance strategy alongside traditional retirement savings. Assume Alex allocates $8,000 annually to a whole life policy designed for cash value accumulation, while contributing $10,000 to the traditional 401(k).

Alex's Modified Strategy:

Traditional 401(k) contribution: $10,000 annually

Whole life insurance premium: $8,000 annually

Combined annual savings: $18,000

The Whole Life Cash Value Projection

Quality whole life insurance policies often project cash value growth in the 4-6% range over the long term. Let's use a conservative 4.5% internal rate of return for Alex's policy.

How Alex's whole life insurance cash value and death benefit grow over 25 years with $8,000 annual premiums. Notice how the policy becomes profitable after year 10, with the "Net Position" showing when cash value exceeds total premiums paid. The death benefit provides substantial protection throughout, growing modestly through dividends while always exceeding the cash value.

By retirement, Alex would have access to approximately $276,800 in cash value, funded by $200,000 in premiums over 25 years.

Tax-Free Retirement Income Through Policy Loans

Here's where the tax advantages become powerful. Instead of taking taxable withdrawals, Alex can borrow against the policy's cash value. These loans are not considered taxable income because technically, you're borrowing your own money using the policy as collateral.

Policy Loan Strategy in Retirement:

How Alex can access retirement income through tax-free policy loans. The "Net Cash Flow" represents spendable income that doesn't count toward Social Security taxation or Medicare premium calculations, providing true tax-free retirement income.

The policy continues to earn dividends on the full cash value, while Alex pays interest only on the borrowed amounts. Many companies offer competitive loan rates, and some policies even have wash loans where the dividend rate equals the loan rate.

Flexible Repayment Terms: Unlike traditional loans, policy loans don't require scheduled payments or have mandatory repayment dates. Alex can choose to repay the loans during retirement to restore the full death benefit, or simply let the loans remain outstanding. Upon Alex's death, any outstanding loan balance plus accrued interest will be deducted from the death benefit paid to beneficiaries, making this truly flexible retirement income without the pressure of loan repayment schedules.

Comparing All Three Strategies: A Side-by-Side Analysis

Let's compare how Alex's retirement income and tax situation would look under each approach:

Year 1 retirement income comparison across all three strategies. This demonstrates how tax diversification affects both gross income and after-tax spendable income, highlighting the hidden costs of traditional 401(k) withdrawals.

Key Insights from the Strategy Comparison

Traditional 401(k) Strategy:

Highest tax burden at 18.2% effective rate

Social Security benefits become taxable due to high provisional income

Medicare surcharges triggered by income above $103,000 threshold

Roth 401(k) Strategy:

Zero taxes on withdrawals

No impact on Social Security taxation

No Medicare premium surcharges

Highest net spendable income

Diversified Strategy:

Lower total income but significantly reduced tax burden

Policy loans provide tax-free income supplement

Maintains flexibility for future tax planning

Preserves death benefit protection

While the diversified strategy produces lower total income in this example, it creates several strategic advantages:

Flexibility and Control: Policy loans can be taken at any age without penalties, providing access to funds before traditional retirement age.

Creditor Protection: In many states, life insurance cash values receive significant protection from creditors, providing an additional layer of asset security.

Legacy Planning: The death benefit provides tax-free wealth transfer to beneficiaries, often exceeding the total premiums paid.

No Market Risk: Unlike 401(k) accounts subject to market volatility, cash value growth is contractually guaranteed with potential for higher returns through dividends.

No Contribution Limits: Unlike 401(k)s and IRAs with annual contribution caps, whole life insurance allows unlimited premium payments, making it valuable for high earners who want to save beyond traditional retirement account limits.

Understanding the Limitations and Considerations

Higher Fees: Life insurance policies carry internal expenses that can impact early cash value accumulation. This is why these strategies work best when maintained for the long term.

Complexity: Properly structuring a policy for retirement income requires working with knowledgeable professionals who understand the tax implications and design requirements.

Modified Endowment Contract (MEC) Rules: Overfunding a policy can trigger MEC status, eliminating many of the tax advantages. Proper design is crucial.

The Enhanced Four-Bucket Strategy

When properly integrated, whole life insurance creates a fourth bucket in your retirement tax diversification strategy:

Optimal Integration Approach:

Traditional accounts for immediate tax relief during peak earning years

Roth accounts for tax-free growth and distributions

Taxable accounts for liquidity and flexibility

Whole life insurance for tax-advantaged income that doesn't affect Social Security or Medicare calculations

This comprehensive approach provides maximum flexibility to manage your effective tax rate throughout retirement by choosing which "bucket" to draw from each year based on your income needs and tax situation.

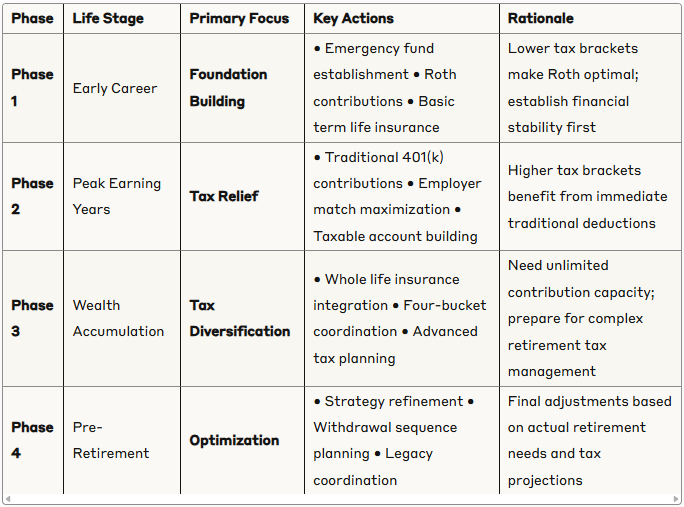

Real-World Implementation: The Phased Approach

Many successful professionals implement this strategy in phases:

Strategic implementation timeline showing when to introduce each component of the four-bucket retirement strategy. This phased approach allows professionals to build complexity gradually as income and financial sophistication increase.

Implementation Benefits by Phase

Phase 1 Benefits:

Maximize decades of tax-free Roth growth

Build emergency protection to avoid retirement account raids

Establish disciplined saving habits

Phase 2 Benefits:

Immediate tax relief during peak earning years

Employer matching maximization

Tax bracket management through traditional contributions

Phase 3 Benefits:

Break through retirement account contribution limits

Add tax-free policy loan capability

Create estate planning coordination opportunities

Phase 4 Benefits:

Fine-tune strategy based on real retirement projections

Coordinate all four buckets for optimal tax efficiency

Prepare for complex retirement income management

Case Study: The Combined Benefits

Let's revisit Alex's lifetime tax picture with a balanced approach using all four buckets:

Modified Allocation:

Traditional 401(k): $10,000 annually

Roth 401(k): $4,000 annually

Whole life Insurance: $8,000 annually

Taxable savings: $2,000 annually

Retirement Income Strategy:

Draw first from taxable accounts for lower capital gains rates

Use policy loans to supplement income without triggering taxes

Take traditional 401(k) withdrawals up to lower tax bracket thresholds

Preserve Roth accounts for later years or legacy planning

This diversified approach provides Alex with multiple tools to optimize tax efficiency each year of retirement while maintaining flexibility to adapt to changing tax laws or personal circumstances.

The Psychology Behind the Traditional 401(k) Trap

Understanding why so many people fall into this trap requires examining the psychological factors at play:

Present Bias

The immediate tax savings from traditional contributions provide instant gratification, while the costs are distant and abstract. A $4,320 tax refund today feels more real than $27,000 in taxes paid twenty-five years from now.

Complexity Aversion

The calculation we just performed requires understanding multiple tax systems and their interactions. Most people understandably prefer the simple narrative of "save taxes now, pay less later."

The "Lower Bracket" Myth

Many assume they'll automatically be in a lower tax bracket during retirement because their salary stops. However, successful retirement planning often maintains or increases income through various sources, potentially keeping tax brackets high or even higher.

Strategic Applications: When Traditional Accounts Still Make Sense

Despite this analysis, traditional retirement accounts aren't always the wrong choice. Several scenarios favor traditional contributions:

Early Retirement Strategies

If you plan to retire early and have several years of low income before Social Security and required minimum distributions begin, traditional accounts can provide tax-efficient withdrawals during those low-income years.

High Current Income with Lower Planned Retirement Spending

If you're currently in a very high tax bracket (32% or 35%) and plan to live on significantly less in retirement, the traditional approach might still be beneficial.

Tax Bracket Management

Having both traditional and Roth accounts provides flexibility to manage your tax bracket each year in retirement by choosing which accounts to withdraw from.

Advanced Strategies: Optimizing Your Tax-Diversified Approach

Now that we understand the four main account types, let's explore sophisticated techniques that professional financial planners use to maximize tax efficiency across your entire retirement strategy.

Roth Conversion Laddering

One of the most powerful advanced strategies involves systematically converting traditional IRA funds to Roth accounts during strategic low-income periods. Think of this as paying taxes at a discount when your rates are temporarily lower.

How Roth Conversion Laddering Works: During years when your income drops below your normal bracket - perhaps during early retirement, career transitions, or market downturns - you can convert traditional IRA funds to Roth accounts. You pay taxes at these lower rates while eliminating future required distributions and Social Security taxation impacts.

Strategic Implementation for Alex: If Alex retires at 60 but delays Social Security until 67, there's a seven-year window where income consists only of investment withdrawals. During these years, Alex could convert $50,000 annually from traditional IRAs to Roth accounts while staying in lower tax brackets.

Dynamic Tax Bracket Management

Advanced retirement income planning involves actively managing your tax bracket each year by strategically choosing which accounts to withdraw from based on your total income picture.

The Bracket-Filling Strategy: Each year, calculate how much income you can take before jumping to the next tax bracket, then "fill up" that bracket with withdrawals from different account types. For instance, you might take enough traditional 401(k) withdrawals to reach the top of the 12% bracket, then switch to Roth or whole life policy loans for additional income needs.

Geographic Arbitrage Considerations: Your choice of retirement location dramatically impacts these calculations. States like Florida, Texas, and Nevada have no state income tax, effectively reducing your total tax burden on traditional account withdrawals. Conversely, states like California or New York can add significant additional taxes to your retirement income.

Sequence of Returns Risk Management

The order in which you withdraw from different account types becomes critical during market downturns. Advanced planners use flexible withdrawal strategies that adapt to market conditions.

Bear Market Protocol: During market downturns, prioritize withdrawals from stable value accounts like whole life cash value or bonds in taxable accounts. This allows your equity investments in retirement accounts to recover without being forced to sell at depressed prices.

Bull Market Protocol: During strong market periods, consider taking larger withdrawals from traditional accounts to execute Roth conversions or to rebalance portfolios while tax rates are known quantities.

Estate Planning Integration

Advanced tax diversification strategies consider not just your lifetime tax efficiency, but also the tax implications for your beneficiaries.

Beneficiary Tax Optimization: Different account types pass to heirs with different tax consequences. Roth accounts provide tax-free inheritance, traditional accounts create taxable income for beneficiaries, and life insurance death benefits transfer tax-free. Strategic account sequencing can minimize your family's total lifetime tax burden.

Generation-Skipping Strategies: Wealthy families often use the tax-free nature of life insurance death benefits combined with trust structures to efficiently transfer wealth across multiple generations while avoiding estate taxes.

Real-World Considerations and Limitations

This analysis makes several assumptions that may not apply to everyone:

Variable Tax Rates

Future tax rates could be higher or lower than today's rates. However, the current federal debt and demographic trends suggest tax rates may increase over time.

State Tax Implications

Some states tax traditional retirement account distributions but not Roth withdrawals. Others have no state income tax at all. Your state of residence during retirement significantly impacts this analysis.

Individual Health and Longevity

The calculations assume a 25-year retirement. Shorter retirements reduce the compounding effect of the tax differences, while longer retirements amplify them.

Changes in Tax Law

Congress could modify Social Security taxation rules, Medicare premium structures, or retirement account regulations. However, planning based on current law remains the most prudent approach.

Action Steps for Different Life Stages

Understanding these retirement tax strategies is valuable, but implementing them requires a systematic approach that evolves with your career and income progression. Think of this as building a financial foundation first, then adding increasingly sophisticated layers as your income and financial complexity grow.

Foundation Stage: Early Career (20s-30s)

During your early career years, your primary focus should be establishing financial stability while taking advantage of your typically lower tax brackets. This stage is about building the groundwork that will support more advanced strategies later.

Step 1: Emergency Fund Foundation Before implementing any retirement tax strategy, establish an emergency fund covering three to six months of expenses. This foundation prevents you from having to withdraw from retirement accounts during financial emergencies, which would undermine your long-term tax planning.

Step 2: Prioritize Roth Contributions Since you are likely in lower tax brackets during these years, Roth contributions provide exceptional value. The decades of tax-free growth ahead of you create tremendous compound benefits. Every dollar you contribute to a Roth account in your twenties has thirty-plus years to grow completely tax-free.

Step 3: Establish Taxable Investment Accounts Once you have maximized available Roth contribution space, begin building taxable investment accounts. These provide flexibility for major life purchases like homes or unexpected opportunities, while also serving as your third bucket for retirement tax diversification.

Step 4: Basic Life Insurance Evaluation Consider term life insurance if you have dependents, but avoid permanent life insurance until your income stabilizes and increases. The exception would be if you have specific estate planning needs or anticipate becoming uninsurable due to health issues.

Building Stage: Mid-Career (40s-50s)

This stage typically brings higher incomes and more complex financial situations. Your strategy should evolve to balance immediate tax benefits with long-term tax diversification across multiple account types.

Traditional vs. Roth Balance Strategy Now that your income has likely increased, the traditional versus Roth decision becomes more nuanced. Consider splitting your contributions based on your current tax bracket and retirement income projections. If you are in the 24% bracket or higher, traditional contributions can provide meaningful immediate tax relief, while continuing some Roth contributions maintains tax diversification.

Maxing Out Retirement Account Limits As your income grows, prioritize maximizing contributions to employer-sponsored retirement plans, especially if your employer provides matching contributions. Once you have maximized these accounts, expand your focus to the remaining buckets in your tax diversification strategy.

Taxable Account Expansion Systematic investing in taxable accounts becomes increasingly important during these years. These accounts provide flexibility for early retirement scenarios, major life transitions, or opportunities that arise before traditional retirement age. Focus on tax-efficient investments like broad market index funds to minimize annual tax drag.

Introduction of Whole Life Insurance For many professionals, this stage represents the optimal time to introduce whole life insurance as a tax diversification tool. Your income has stabilized and grown, you understand your long-term financial needs better, and you have decades ahead to allow the cash value to develop effectively.

Optimization Stage: Peak Earning Years (50s-60s)

During your highest earning years, your strategy should focus on maximizing tax efficiency while preparing for the transition to retirement income distribution.

Advanced Whole Life Insurance Implementation If you have maximized traditional retirement account contributions and still want to save additional funds with tax advantages, properly structured whole life insurance becomes particularly valuable. The unlimited contribution capacity helps high earners who bump against 401(k) and IRA limits, while the tax-free policy loan access provides another tool for managing retirement income taxes.

Comprehensive Tax Bucket Management At this stage, you should be actively managing all four buckets based on your annual tax situation. High-income years might favor traditional contributions and whole life premiums, while any lower-income years present opportunities for Roth conversions or increased taxable account funding.

Pre-Retirement Tax Planning Begin modeling different withdrawal strategies to understand how your four-bucket approach will work in practice. Consider working with tax professionals to run scenarios that account for Social Security taxation, Medicare premium surcharges, and required minimum distributions from traditional accounts.

Estate Planning Integration Your whole life insurance strategy should coordinate with broader estate planning goals. The death benefit provides tax-free wealth transfer opportunities, while the cash value offers flexibility during your lifetime.

Transition Stage: Pre-Retirement (55-65)

The years immediately before full retirement require careful coordination of your various account types to optimize your transition from accumulation to distribution.

Roth Conversion Opportunities If you retire before claiming Social Security, you may have several years with lower income that create excellent opportunities for Roth conversions. Converting traditional IRA funds during these years allows you to pay taxes at temporarily reduced rates while eliminating future required minimum distributions.

Bridge Strategy Implementation Plan how different account types will provide income during various phases of retirement. You might use taxable accounts and whole life policy loans during early retirement years, begin Social Security at your optimal claiming age, and delay traditional retirement account withdrawals as long as possible to minimize the cumulative effect of required distributions.

Required Minimum Distribution Planning If you have significant traditional retirement account balances, develop a strategy for managing required minimum distributions that begin at age 73. Consider how these mandatory withdrawals will interact with Social Security taxation and Medicare premium calculations.

Distribution Stage: Retirement

During retirement, your four-bucket strategy transitions from accumulation to sophisticated income coordination designed to minimize your lifetime tax burden.

Dynamic Withdrawal Sequencing Rather than following rigid withdrawal rules, optimize your income sources year by year based on your total financial picture. Some years might favor traditional account withdrawals to fill lower tax brackets, while other years might emphasize tax-free sources like Roth distributions or whole life policy loans.

Social Security and Medicare Coordination Carefully coordinate your withdrawal timing and amounts with Social Security claiming strategies and Medicare premium calculations. Remember that Roth withdrawals and whole life policy loans do not count toward the income calculations that trigger Social Security taxation or Medicare premium surcharges.

Market Condition Adaptation Adapt your withdrawal strategy based on market conditions. During market downturns, prioritize stable value sources like whole life cash value or bond portions of taxable accounts, allowing equity investments in retirement accounts to recover without forced selling at depressed prices.

Legacy Planning Execution Coordinate the timing of distributions with estate planning goals. Roth accounts and life insurance death benefits provide the most tax-efficient wealth transfer opportunities, while traditional accounts create taxable income for beneficiaries.

The key insight throughout all these stages is that effective retirement tax planning is not about finding the single best account type, but rather about building a diversified system that provides flexibility to adapt to changing tax laws, life circumstances, and financial markets while minimizing your total lifetime tax burden.

The Bottom Line: Challenging Conventional Wisdom

The traditional 401(k) deduction isn't actually saving you money - it's deferring taxes to a time when you may pay significantly more. This analysis reveals why the conventional wisdom of "you'll be in a lower tax bracket in retirement" deserves serious scrutiny.

The key insight isn't that traditional retirement accounts are bad, but rather that the decision requires careful analysis of your complete lifetime tax picture. For many people, paying taxes at known rates today proves more beneficial than paying unknown (and potentially much higher) effective rates in retirement.

Consider this: would you rather pay income tax on the seed or the harvest? When that seed grows into a tree that produces fruit for decades, the harvest becomes substantially larger than the original seed. The same principle applies to your retirement savings.

The most important step you can take is to run these calculations for your specific situation. Consider your current income, expected retirement lifestyle, state tax implications, and other personal factors. What you discover might fundamentally change your approach to retirement savings.

Remember, the goal of retirement planning isn't to minimize taxes today - it's to maximize your after-tax income when you need it most: during retirement.

Disclaimer

This article is for educational and informational purposes only and should not be considered personalized financial, tax, or investment advice. Tax laws are complex and subject to change, and individual circumstances vary significantly. The examples and calculations presented are hypothetical and may not reflect actual investment returns, tax rates, or personal situations.

Before making any financial decisions, please consult with qualified financial advisors, tax professionals, and/or estate planning attorneys who can provide guidance based on your specific circumstances. Past performance does not guarantee future results, and all investments carry risk of loss.

The author makes no guarantees about the accuracy of the information presented, and readers should verify all tax rules and calculations with current tax law and professional advisors. Social Security, Medicare, and tax regulations are subject to change by Congress and may differ from the assumptions used in this analysis.

This content is not intended to provide specific advice to any individual and should not be relied upon as the sole basis for financial planning decisions.

Social Security Taxation Thresholds