- The Strategic Tax Advisor

- Posts

- The $100/Month Decision That Could Change Your Child's Financial Life

The $100/Month Decision That Could Change Your Child's Financial Life

A whole life policy started at birth quietly builds a financial toolkit your child will use to pay for college, buy a home, and retire with confidence — all from a single monthly premium you probably won't notice.

Prashanth Srikanthan

March 20, 2026

Most parents think about life insurance on a child and immediately ask the wrong question:

"Why would I insure someone who doesn't have an income to replace?"

That question misses the point entirely. Insuring a child through whole life insurance is not about income replacement. It is about locking in 3 specific financial advantages, permanently, at the lowest possible cost, before life gets in the way.

The 3 Core Reasons to Insure a Child

1. Future insurability protection A chronic illness diagnosis at age 19 can lock a young adult out of affordable life insurance coverage for life. Diabetes, Crohn's disease, depression, and dozens of other manageable conditions are enough to trigger rated policies or outright declines. A policy started today eliminates that risk permanently. The coverage is locked in regardless of what health events follow.

2. A growing financial asset Cash value accumulates tax-deferred inside a whole life policy and is accessible — without credit checks, without application processes, and for any purpose — at the exact life milestones when your child will need it most: college graduation, a first home purchase, starting a business.

3. A generational legacy A death benefit that passes entirely tax-free creates a multi-generational financial habit. For many families, this is where the legacy of financial planning begins.

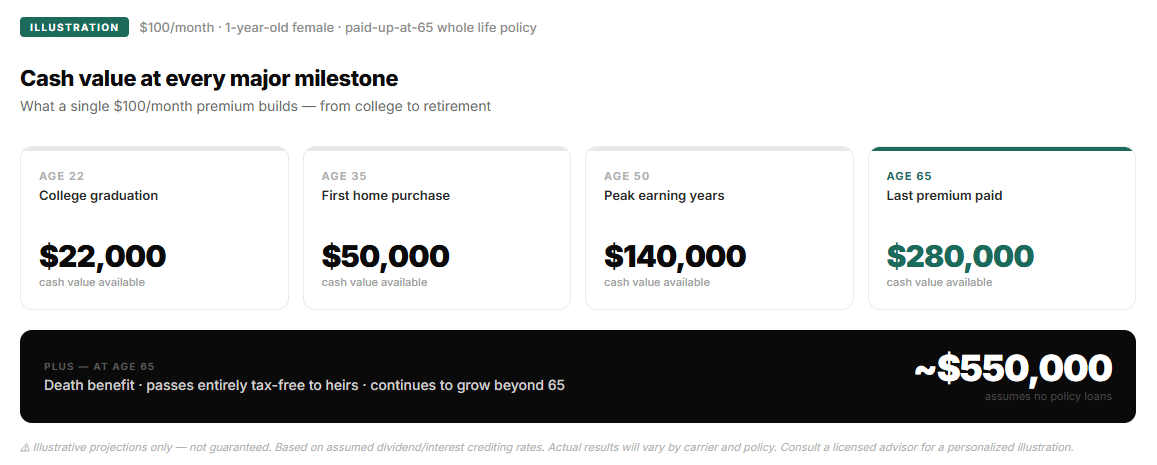

The Math: What $100/Month Actually Builds

Let us look at a concrete example. A paid-up-at-65 whole life policy issued on a 1-year-old female, starting at just $100 per month.

Right away, this child is insured for over $200,000 in death benefit. But the real story plays out across every major financial milestone in her life.

Here is how those milestones break down:

Life Milestone | Age | Cash Value Available |

|---|---|---|

College graduation | 22 | ~$22,000 |

First home purchase | 35 | ~$50,000 |

Peak earning years | 50 | ~$140,000 |

Last premium paid — retirement | 65 | ~$280,000 |

And the death benefit at age 65, assuming no policy loans? Approximately $550,000 — passing entirely tax-free to heirs. The policy continues to grow beyond age 65.

"At $100 a month — less than a daily coffee — a parent can build a financial toolkit their child will still be drawing from at retirement."

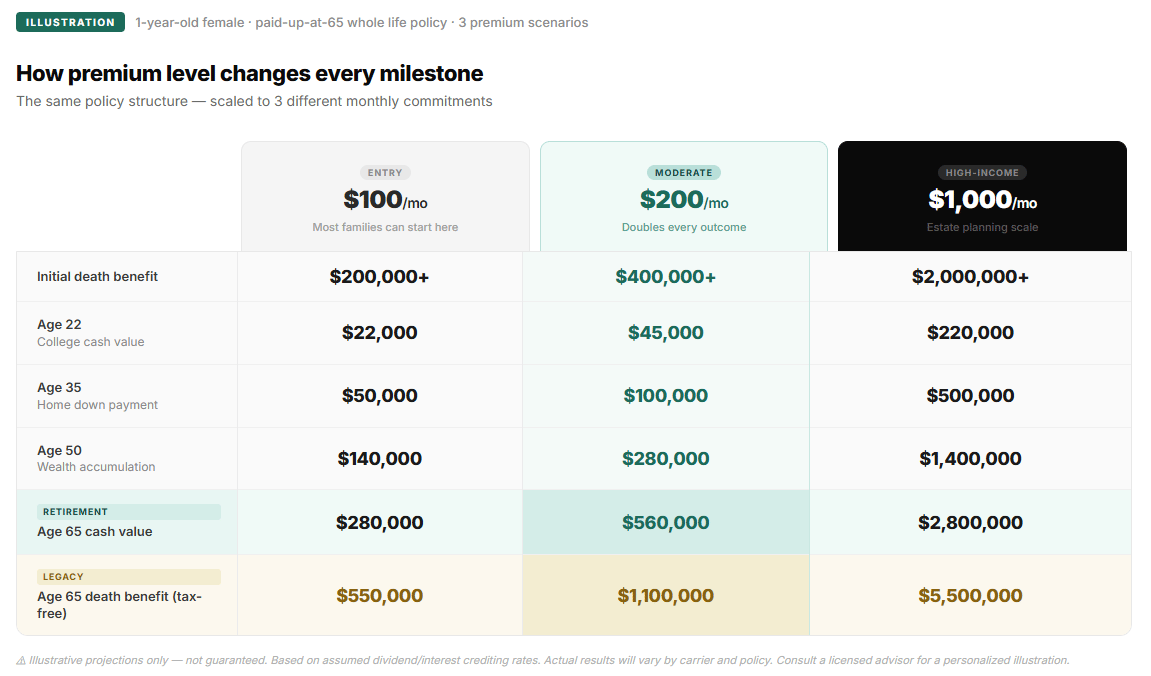

The $100/month example is the floor. The same policy structure scales proportionally. Here is how 3 premium levels compare at each major milestone for the same 1-year-old female.

⚠️ Values are illustrative projections based on assumed dividend/interest crediting rates and are not guaranteed. Actual results will vary. Consult a licensed advisor for a policy-specific illustration.

What does $45,000 at age 22 actually mean in practice? Federal student loan interest rates currently range from 6.5% to over 8%. A policy loan is typically available at a lower rate with no fixed repayment schedule. Borrowing ~$40,000 from the policy at age 22 to pay down high-interest student debt — and repaying it flexibly over 5 years — is a real wealth-building strategy, not just a talking point.

What does $100,000 at age 35 actually mean? In most U.S. markets, $100,000 represents a full down payment on a median-priced home. It arrives with no bank involved, no credit check, and no approval timeline — at exactly the moment your child's family is ready to buy.

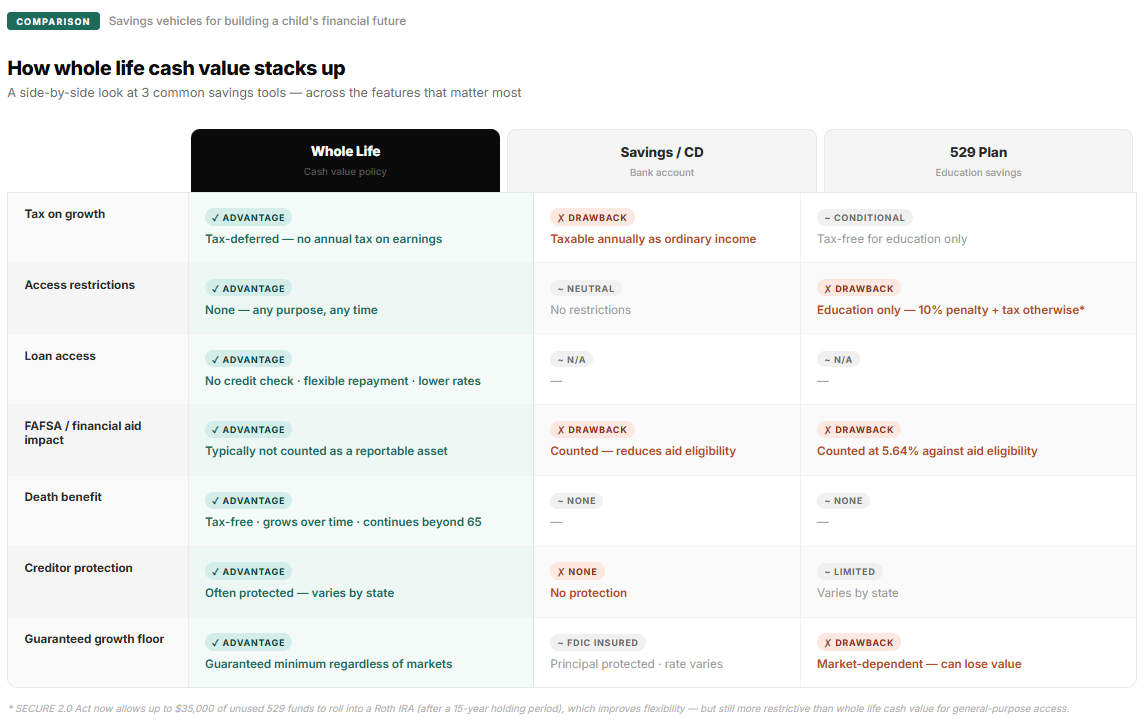

How the Cash Value Actually Works

Cash value in a whole life policy is not the same as money in a savings account. It behaves differently — and in several ways, it behaves better.

* 529 funds can now be rolled into a Roth IRA (up to $35,000 lifetime, after a 15-year holding period) per SECURE 2.0 Act rules, which improves flexibility — but still not as flexible as whole life cash value for general use.

The Policy Loan: A Misunderstood Tool

The most powerful — and least understood — feature of whole life cash value is the policy loan. Here is exactly how it works.

You borrow against your cash value, not from it. The cash value stays in the policy, continuing to earn dividends. The insurance company lends you an equivalent amount at the policy loan rate. You are not depleting the asset — you are leveraging it.

No credit check. No application. No approval process. The cash value is the collateral. If sufficient value exists, the loan is available. This matters enormously at age 22 when credit history is thin or nonexistent.

No mandatory repayment schedule. You can repay on your own timeline. Unpaid loan balances will reduce the death benefit over time, but there is no default event that triggers credit damage or legal consequences.

Interest rates are typically lower than consumer alternatives. Policy loan rates — often in the 5–6% range — compare favorably to private student loans, personal loans, and credit card debt. And unlike a bank loan, the interest effectively stays within your financial ecosystem.

Addressing the Real Objection: "It's Too Expensive"

The most common pushback from parents is that premiums feel like a burden with no immediate payoff. Here is the context that reframes that.

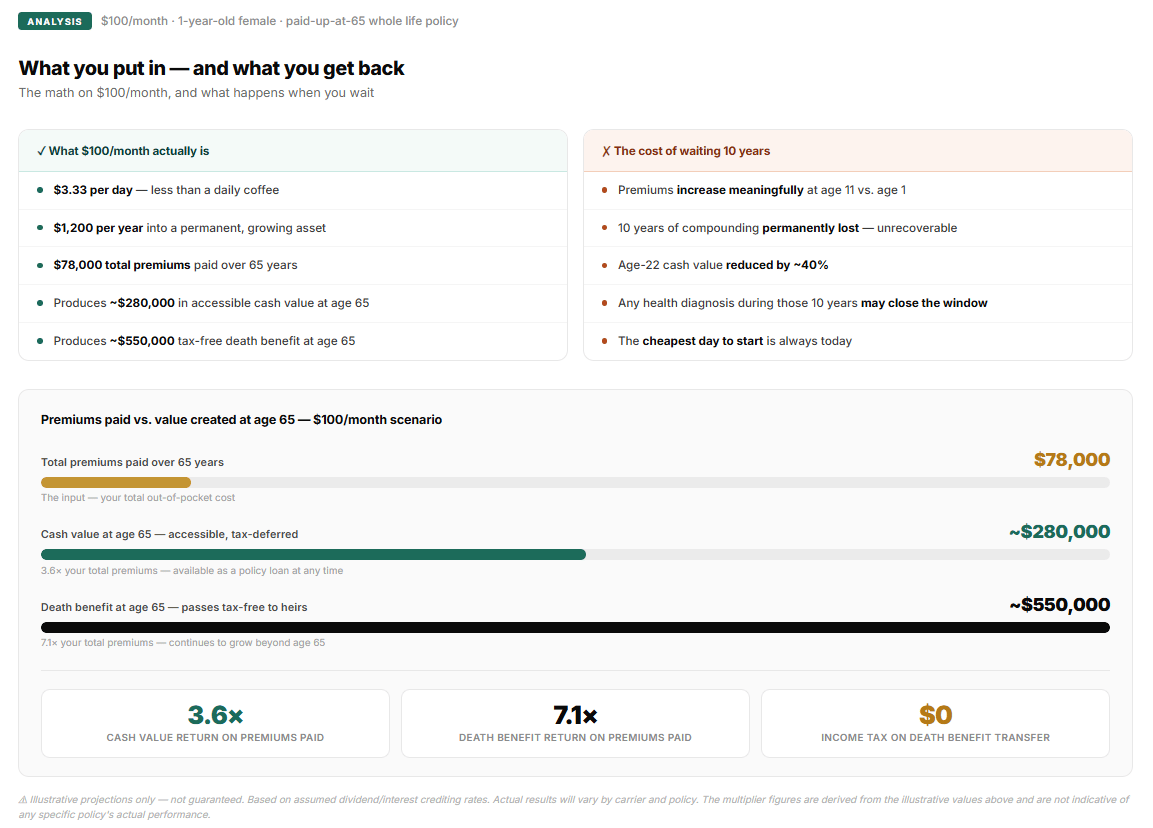

What $100/month actually is:

$3.33 per day — less than a daily coffee

$1,200 per year in premiums that lock in permanent coverage and build cash value over time

$78,000 in total premiums paid over 65 years

Results in ~$280,000 in accessible, tax-deferred cash value at age 65

Results in ~$550,000 in tax-free death benefit

The cost of waiting 10 years:

Premiums increase meaningfully at older issue ages

10 years of compounding are permanently lost — they cannot be recovered

The age-22 cash value is reduced by roughly 40%

If the child develops a health condition in those 10 years: coverage may be unavailable

The cheapest day to start is always today

Is This the Right Move for Your Family?

Whole life insurance for children is not appropriate for every family. Here is a straightforward framework.

Your Situation | Fit? | Why |

|---|---|---|

Parents are already adequately insured | ✅ Strong fit | Juvenile policy is complementary — not a substitute for parental coverage |

Family history of chronic illness | ✅ Strong fit | Locks in insurability before any diagnosis affects underwriting |

High-income family with estate planning focus | ✅ Strong fit | Policy scales well; death benefit becomes a meaningful estate tool |

Parents underinsured or no emergency fund | ⚠️ Address first | Parent coverage and a 3–6 month emergency fund should come first |

Very tight cash flow | ⚠️ Timing matters | The right premium level should not create financial stress; start smaller or delay |

Child with an existing health condition | ⚠️ Case-specific | May still be insurable — underwriting is evaluated individually; worth a conversation |

Want to See Your Child's Numbers?

Every family's situation is different. I can run a personalized illustration showing exactly what a policy started today would look like at every milestone — college, home purchase, and retirement.

Disclosure: The illustrations and projections in this article are hypothetical examples intended for educational purposes only, based on assumed dividend crediting rates. They are not guaranteed. Actual policy performance will vary by carrier, policy type, dividend scale, and individual underwriting. This content does not constitute financial, tax, or legal advice. Consult a licensed insurance and financial advisor before making any insurance purchasing decisions.