- The Strategic Tax Advisor

- Posts

- The Big Beautiful Bill's tax impact on high earners

The Big Beautiful Bill's tax impact on high earners

A Strategic Guide to Tax Savings, Effective Rate Reductions, and Planning Opportunities Under the 2025 Legislation

Prashanth Srikanthan

July 20, 2025

The "One Big Beautiful Bill Act" signed into law July 4, 2025, represents a significant preservation of existing tax advantages for high earners rather than introducing new tax increases. The legislation prevents the top marginal tax rate from reverting to 39.6% and keeps it permanently at 37%, while introducing several targeted provisions that primarily benefit wealthy taxpayers through enhanced deductions and permanent rate structures.

President Trump signed this massive budget reconciliation package during Independence Day celebrations at the White House, following narrow congressional passage (51-50 in the Senate with VP Vance's tiebreaking vote, 218-214 in the House). The legislation makes permanent the 2017 Tax Cuts and Jobs Act individual provisions that were set to expire in 2025, while adding new deductions and maintaining favorable treatment for high earners.

What exactly is the Big Beautiful Bill

Official designation: The "One Big Beautiful Bill Act" (OBBBA), formally designated as H.R. 1 of the 119th Congress and Public Law 119-21, passed Congress July 1-3, 2025. This nearly 1,000-page budget reconciliation package represents President Trump's centerpiece domestic legislation, incorporating $3.4 trillion in deficit spending over 10 years while cutting $4.46 trillion in tax revenue.

The legislation combines tax policy changes with significant spending provisions, including $150 billion for defense, $175 billion for immigration enforcement, and substantial cuts to social programs like Medicaid and SNAP. For tax purposes, the bill's core achievement is making permanent the individual provisions of the 2017 Tax Cuts and Jobs Act while adding several new deductions that predominantly benefit higher-income taxpayers.

Note: This analysis focuses specifically on the tax provisions affecting high earners. The Big Beautiful Bill contains numerous other provisions affecting healthcare, immigration, education, and other policy areas. If you'd like me to provide a detailed analysis of any specific provision mentioned in this post—such as the QSBS changes, AMT modifications, or estate tax implications—please let me know and I can do a comprehensive deep dive on that topic.

No new marginal tax rates for high earners

The legislation preserves rather than increases tax rates for wealthy Americans. Understanding how these rates apply requires examining both current brackets and what they would have become without this legislation. Let's break this down systematically to see the true impact on high earners.

Current Tax Brackets Preserved (2025 and Beyond)

Federal tax brackets remain unchanged under the Big Beautiful Bill, preserving the lower rates established by the 2017 Tax Cuts and Jobs Act

What Rates Would Have Been Without the Big Beautiful Bill

Comparison showing how tax rates would have increased in 2026 without the legislation—note the 2.6% savings for top earners

This table reveals the legislation's most significant impact: preventing the top marginal rate from jumping to 39.6% for the highest earners. While those earning $400,000-$750,000 see modest benefits, earners above $750,000 receive the most substantial protection from rate increases.

Effective tax rate implications reveal significant savings

Understanding marginal rates tells only part of the story. The true financial impact becomes clear when we examine effective tax rates—the percentage of total income actually paid in taxes. Tax Foundation analysis shows high earners experience meaningful reductions through the permanent rate structure.

After-Tax Income Increases by Income Percentile

Higher-income groups see the largest percentage increases in after-tax income under the new legislation

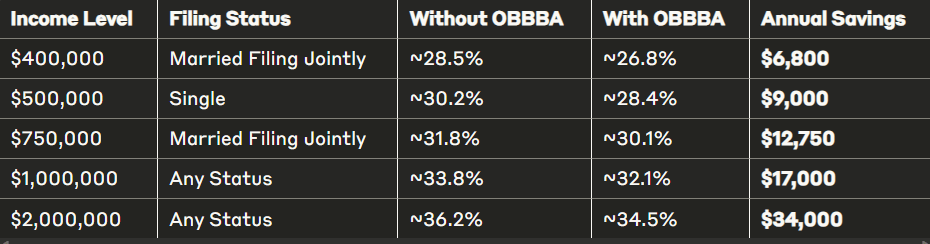

Effective Tax Rate Examples: Before vs. After OBBBA

Real dollar savings for different income levels—notice how the annual savings compound significantly over time

These savings represent permanent annual reductions that compound over time. A high earner saving $17,000 annually would accumulate $170,000 in tax savings over just ten years, not accounting for investment growth on those preserved funds.

Enhanced deductions benefit high earners strategically

The legislation introduces several deduction changes that create both opportunities and limitations for wealthy taxpayers. Understanding these provisions requires examining how they interact with income levels and other tax provisions.

State and Local Tax (SALT) Deduction Changes

Temporary increase in SALT deduction cap with phase-out for ultra-high earners—maximizes benefit for those in high-tax states

This provision particularly benefits high earners in states like California, New York, and New Jersey, where property and state income taxes often exceed the previous $10,000 limit. However, the phase-out mechanism ensures ultra-high earners (above $500,000 MAGI) receive reduced benefits.

Alternative Minimum Tax (AMT) Threshold Changes

What is the Alternative Minimum Tax? The AMT is a parallel tax system designed to ensure high earners pay a minimum amount of tax, even after claiming deductions and credits. It operates by calculating taxes under different rules (adding back certain deductions and applying AMT rates of 26% and 28%) and requiring taxpayers to pay whichever amount is higher—regular tax or AMT. The AMT particularly affects high earners who claim significant deductions for state taxes, depreciation, or incentive stock options.

How AMT exemptions work: Taxpayers can exclude a certain amount of income from AMT calculations (the "exemption"), but this exemption phases out as income rises, effectively creating higher marginal tax rates during the phase-out range.

The legislation creates a more complex AMT landscape starting in 2026, with tighter phase-out ranges that create higher effective marginal rates for certain income levels.

Lower phase-out thresholds starting in 2026 create higher effective tax rates during the transition ranges—plan Incentive Stock Option (ISO) exercises accordingly

New Deduction Limitations for High Earners

Starting in 2026, several new limitations specifically target the highest income brackets:

Starting in 2026, new restrictions target the highest income brackets—note how charitable giving and itemized deductions become less valuable

Permanent estate tax advantages and business benefits

Long-term wealth building and preservation: While many tax provisions are temporary, this section covers the legislation's most significant permanent benefits for high earners. These changes fundamentally alter long-term tax planning by expanding opportunities for wealth accumulation (through business investments) and wealth transfer (through estate planning).

Why "permanent" matters: Unlike the temporary SALT deduction increases or other sunset provisions, these changes don't expire. This permanence allows high earners to build multi-decade strategies around enhanced estate exemptions and business tax advantages without worrying about future legislative changes.

Targeting wealth creation and transfer: The provisions work together strategically—QSBS benefits help entrepreneurs and investors build wealth tax-efficiently, while expanded estate exemptions help transfer that wealth to heirs. Business provisions provide immediate cash flow benefits that can fund further investments or estate planning strategies.

The legislation provides substantial long-term benefits for wealthy families through enhanced estate planning opportunities and expanded business tax advantages. These changes represent some of the most significant wealth preservation tools in the new law.

Estate Tax Exemption Changes

Understanding estate taxes and exemptions: The federal estate tax applies to the transfer of wealth when someone dies, but only estates above certain thresholds pay this tax. The "exemption" is the amount of wealth that can be transferred tax-free to heirs. For amounts above the exemption, estates pay a 40% federal tax rate—making these exemption increases extremely valuable for wealthy families.

Why exemption amounts matter: Higher exemptions mean more wealth can pass to the next generation without triggering estate taxes. The increases in this legislation are particularly significant because they prevent a dramatic reduction in exemptions that was scheduled to occur when the Tax Cuts and Jobs Act provisions expired.

Dramatic increases in estate tax exemptions allow wealthy families to transfer significantly more wealth tax-free to heirs

This change significantly benefits wealthy families by allowing substantially more wealth to transfer tax-free to heirs. A couple can now pass $30 million without federal estate tax, compared to the $14 million that would have been available after TCJA expiration.

Qualified Small Business Stock (QSBS) Enhanced Benefits

What is Qualified Small Business Stock? QSBS is a powerful tax incentive designed to encourage investment in small businesses. When you hold qualifying stock for at least five years, you can exclude up to $10 million (or 10x your basis, whichever is greater) of capital gains from federal taxes—essentially making those gains tax-free. This represents one of the most significant tax advantages available to investors and entrepreneurs.

Who benefits from QSBS? Primarily startup founders, early employees receiving stock options, and angel investors who invest in qualifying small businesses. The tax savings can be enormous—on a $10 million gain, QSBS treatment saves approximately $2.4 million in federal capital gains taxes (assuming the 20% rate plus 3.8% net investment income tax).

Key requirements for QSBS: The company must be a C-corporation with gross assets under certain thresholds, conduct an active business (not passive investments), and meet other technical requirements. The stock must be acquired directly from the company and held for at least five years.

The legislation dramatically expands QSBS advantages for business owners and investors, creating a tiered system based on holding periods:

New tiered exclusion system rewards longer holding periods—5+ years now provides complete tax elimination on qualifying gains

Business Asset Thresholds and Requirements

Understanding QSBS qualification rules: For stock to qualify as Qualified Small Business Stock, the underlying company must meet specific size requirements both when the stock is issued and throughout the holding period. The "business asset threshold" refers to the maximum value of company assets that still allows QSBS treatment—if a company grows beyond this limit, newly issued stock loses QSBS eligibility.

Why these thresholds matter: Higher thresholds mean larger, more mature companies can still issue QSBS-eligible stock to new investors and employees. This is particularly valuable for rapidly growing startups that might have previously "outgrown" QSBS eligibility before reaching major liquidity events.

Raised thresholds allow larger companies to still qualify for QSBS benefits—expanding opportunities for growing businesses

Additional Business Provisions

Understanding key business tax benefits: These provisions create immediate cash flow advantages for business owners by allowing faster or more generous tax deductions for business investments and expenses.

100% Bonus Depreciation allows businesses to immediately deduct the full cost of qualifying property (machinery, equipment, etc.) in the year it's purchased, rather than spreading the deduction over multiple years. This creates substantial upfront tax savings and improves cash flow for growing businesses.

R&D Expense Treatment determines when businesses can deduct research and development costs. "Immediate domestic expensing" means companies can deduct these expenses right away rather than capitalizing and amortizing them over 5-15 years. This is particularly valuable for technology companies and innovative businesses.

Section 179 Expensing allows small to mid-sized businesses to immediately deduct the cost of qualifying equipment purchases up to a specified dollar limit, rather than depreciating them over time. Higher limits mean larger businesses can take advantage of this immediate deduction.

Immediate cash flow benefits for business owners through accelerated deductions and permanent expensing opportunities

These business provisions create immediate cash flow benefits for companies and business owners, while the QSBS changes provide long-term wealth accumulation opportunities for entrepreneurs and investors willing to hold qualifying stock for extended periods.

Implementation timeline creates planning opportunities

Understanding when different provisions take effect becomes crucial for tax planning strategies. The legislation creates a complex implementation schedule that requires careful attention to timing for optimal benefit.

Retroactive Provisions (Effective January 1, 2025)

New deductions that apply to 2025 income—note how income phase-outs limit benefits for higher earners

Most of these retroactive deductions phase out at income levels that eliminate benefits for earners above $400,000, making them largely irrelevant for high-income taxpayers.

Major Changes by Implementation Date

Understanding the staggered rollout: The Big Beautiful Bill doesn't implement all changes at once. Instead, it creates a complex timeline with retroactive provisions, immediate changes, and future effective dates. This staggered approach means different tax strategies become optimal at different times.

Why implementation timing affects planning: Some benefits are already available (retroactive to January 1, 2025), others start immediately, and key provisions don't begin until 2026. Understanding this timeline helps prioritize which planning strategies to implement first and which to prepare for future years.

Reading the impact levels: The "High Earner Impact" column indicates which changes matter most for taxpayers above $400,000. "High" impact provisions typically save significant money or require immediate action, while "Low" impact items may have income phase-outs that eliminate benefits for wealthy taxpayers.

Strategic timeline showing when each provision takes effect—use this to sequence your tax planning decisions for maximum benefit

Critical Planning Deadlines for High Earners

Why timing matters in tax planning: The Big Beautiful Bill creates both temporary opportunities and permanent changes that require strategic timing to maximize benefits. Some provisions offer limited-time advantages, while others create new restrictions that make current planning more valuable.

Strategic windows of opportunity: High earners face a unique situation where acting before certain deadlines can lock in significant tax advantages or avoid increased costs. Missing these deadlines could mean forgoing tens of thousands in tax savings or facing higher effective rates on future transactions.

The cost of waiting: Unlike standard tax planning that follows annual cycles, these legislative changes create one-time transition periods. For example, exercising stock options before AMT thresholds tighten could save thousands in taxes, while waiting could permanently increase the tax cost of the same transaction.

Time-sensitive action items that could save tens of thousands in taxes—missing these deadlines means permanently forgoing opportunities

The implementation timeline reveals a strategic opportunity window. High earners should focus on maximizing benefits during the 2025-2029 period while preparing for the permanent changes that take effect in 2026. The temporary nature of some provisions, particularly the enhanced SALT deduction, creates urgency around certain planning decisions.

Conclusion

The "One Big Beautiful Bill Act" fundamentally preserves and enhances tax advantages for high earners rather than implementing progressive rate increases. By preventing the reversion to 39.6% top rates and adding beneficial provisions like expanded SALT deductions, enhanced estate tax exemptions, and permanent business advantages, the legislation creates substantial ongoing tax savings for wealthy Americans. The effective result is a tax system that becomes more favorable to high earners compared to what would have occurred without the legislation, despite the "progressive" framing around marginal tax rates. High-earning taxpayers should focus on maximizing temporary benefits while planning for permanent advantages that take effect in 2026.

Disclaimer: This analysis is provided for educational purposes only and should not be considered personalized tax, legal, or financial advice. Tax laws are complex and individual circumstances vary significantly. The information presented reflects the provisions of the One Big Beautiful Bill Act as understood at the time of publication, but tax legislation can be subject to interpretation, regulation changes, and future amendments. Before making any financial decisions or implementing tax strategies mentioned in this post, please consult with qualified tax professionals, estate planning attorneys, or financial advisors who can evaluate your specific situation and provide personalized guidance appropriate to your circumstances.