- The Strategic Tax Advisor

- Posts

- Understanding Trump Accounts: A Complete Guide to America's New Children's Investment Program

Understanding Trump Accounts: A Complete Guide to America's New Children's Investment Program

How to Claim Your Child's $1,000 Government Gift and Build Long-Term Wealth Through Strategic Tax-Deferred Investing

Prashanth Srikanthan

August 15, 2025

In July 2025, President Trump signed into law the "One Big Beautiful Bill," which included a provision that has captured the attention of parents and financial advisors nationwide. The legislation creates new investment accounts for children under 18, with the government providing $1,000 in seed money for U.S. citizens born between 2025 and 2028. While these accounts have been nicknamed "Trump accounts" by Republican lawmakers, they represent something much more significant than their political branding suggests.

Important timing note: Although the law was signed in July 2025, Trump accounts are expected to become available for opening starting in 2026. This gives financial institutions time to set up the infrastructure needed to offer these accounts and allows the IRS to issue detailed implementation guidance.

Let's dive deep into how these accounts work, who can benefit from them, and how they compare to other savings strategies you might already be familiar with.

What Are Trump Accounts, Really?

Think of Trump accounts as a hybrid between a traditional IRA and a college savings plan, but with some unique characteristics that set them apart from both. At their core, Trump accounts are tax-deferred retirement accounts specifically designed for American children, but they're structured to be more accessible than traditional retirement accounts.

The fundamental concept is elegantly simple: give every American child a financial stake in the country's economic success from birth, allowing them to benefit from compound growth over nearly two decades before they even enter the workforce.

The $1,000 Head Start: More Valuable Than You Might Think

Children born between January 1, 2025, and December 31, 2028, automatically qualify for a $1,000 deposit from the U.S. Treasury. This might not sound like a fortune, but let's put the power of compound growth into perspective.

Let's look at the real numbers to understand just how powerful this $1,000 head start can be:

Table 1: The Power of the Government's $1,000 Seed Money. How a single $1,000 government contribution grows over a lifetime with no additional investments

This table demonstrates the magic of starting early – time becomes your most powerful ally in building wealth. Even if you never add another penny to the account, that government-funded $1,000 essentially provides your child with a significant retirement nest egg, completely free of charge.

But let's consider what happens when parents maximize their contributions. If you contribute the full $5,000 annually for 18 years (totaling $90,000 in contributions plus the government's $1,000), here's how the account could grow:

Table 2: Government Seed Money vs. Maximum Family Contributions. Comparing the long-term impact of claiming only the free $1,000 versus maximizing annual contributions

This demonstrates why these accounts have captured so much attention – consistent contributions over time can indeed create substantial wealth.

How Contributions Work: Building Beyond the Foundation

Parents can contribute up to $5,000 per year to their child's Trump account, and this limit will be adjusted for inflation starting in 2027. Importantly, there's no requirement that the child have any earned income to receive these contributions, unlike traditional or Roth IRAs. This removes a major barrier that previously prevented parents from starting retirement savings for very young children.

Here's where it gets interesting for families: employers can also contribute up to $2,500 per year to an employee's child's account, and this contribution won't count as taxable income to either the parent or child. Let's see how this could work in practice:

Example: The Johnson Family

Sarah works for a tech company that offers Trump account contributions as a benefit

She has two children, ages 5 and 8

Her employer contributes $2,500 per child annually

Sarah adds $2,500 of her own money per child to reach the $5,000 maximum

Total annual family contribution: $10,000 across both children

Sarah's tax benefit: She avoids paying income tax on the $5,000 in employer contributions

This arrangement provides meaningful value to both the employer (who gets a business tax deduction) and the employee (who receives tax-free benefits). We might start seeing Trump account contributions offered alongside health insurance and 401(k) matches as part of competitive employee benefit packages.

For business owners, this creates an even more compelling opportunity. Consider this scenario:

Example: Small Business Owner Strategy

Mark owns a small consulting firm with 10 employees

Each employee has an average of 1.5 children eligible for Trump accounts

Mark offers $2,000 per child as an employee benefit (below the $2,500 maximum)

Annual cost to business: $30,000 (15 children × $2,000)

Tax deduction for business: $30,000

Employee value: Each family receives $2,000-4,000 in tax-free benefits annually

Employee retention benefit: Provides meaningful long-term value that employees appreciate

Investment Rules: Simplicity by Design

Trump account funds must be invested in low-cost index funds that track major U.S. stock indexes like the S&P 500. While this might seem restrictive compared to other investment accounts, there's wisdom in this constraint.

The requirement serves several purposes. First, it ensures that families can't make poor investment choices that could devastate their children's accounts. Second, it guarantees low fees, which can significantly impact long-term returns. Third, it ties every participating child's financial future to the broader success of American businesses, creating a shared stake in the country's economic prosperity.

After the child turns 18, the investment restrictions may be relaxed, allowing the account holder to invest in the same range of options available within traditional IRAs.

Access Rules: When and How the Money Can Be Used

The money is completely untouchable until the child reaches 18 years old. This might seem restrictive, but it serves an important purpose: it prevents the accounts from being raided for non-essential expenses during the child's formative years.

Once the child turns 18, the account follows traditional IRA withdrawal rules. Let me walk you through exactly what this means with concrete examples of how withdrawals work in different situations.

Understanding the Withdrawal Structure

Trump account distributions follow what's called the "pro-rata rule," which means each withdrawal contains a mix of contributions (tax-free) and earnings (taxable). Here's how this works in practice:

Example: Sarah's Trump Account at Age 22

Total account value: $50,000

Original contributions (including government seed): $35,000

Earnings: $15,000

Contribution percentage: 70% ($35,000 ÷ $50,000)

Earnings percentage: 30% ($15,000 ÷ $50,000)

If Sarah withdraws $10,000 for any purpose:

Tax-free portion (contributions): $7,000 (70% of withdrawal)

Taxable portion (earnings): $3,000 (30% of withdrawal)

Income tax owed on $3,000 at her tax rate

Potential 10% penalty: $300 (if withdrawal doesn't qualify for exception)

Penalty-Free Withdrawal Exceptions

The good news is that several common life events allow penalty-free early withdrawals, though the earnings portion remains subject to income tax. Here's a comprehensive breakdown:

Table 3: Trump Account Early Withdrawal Rules and Exceptions. When you can access your money before retirement age and what it costs

Let me illustrate how these rules play out through several realistic scenarios:

Scenario 1: College Student

Alex is 20 years old and needs $15,000 for his junior year college expenses. His Trump account has $45,000 total ($30,000 contributions, $15,000 earnings).

Withdrawal Calculation:

Withdrawal amount: $15,000

Tax-free portion: $10,000 (66.7% contributions ratio)

Taxable earnings: $5,000 (33.3% earnings ratio)

Penalty: $0 (education exception applies)

Income tax owed: $5,000 × his tax rate (likely 12% = $600)

Net proceeds: $14,400

Scenario 2: First-Time Homebuyer

Jessica is 25 and wants to buy her first home. She needs $8,000 for a down payment. Her Trump account has $62,000 ($42,000 contributions, $20,000 earnings).

Withdrawal Calculation:

Withdrawal amount: $8,000

Tax-free portion: $5,419 (67.7% contributions ratio)

Taxable earnings: $2,581 (32.3% earnings ratio)

Penalty: $0 (first-home exception applies)

Income tax owed: $2,581 × 22% (her tax bracket) = $568

Net proceeds: $7,432

Scenario 3: Emergency Withdrawal (No Exception)

Michael is 24 and faces an unexpected financial emergency requiring $12,000. His Trump account has $55,000 ($38,000 contributions, $17,000 earnings).

Withdrawal Calculation:

Withdrawal amount: $12,000

Tax-free portion: $8,291 (69.1% contributions ratio)

Taxable earnings: $3,709 (30.9% earnings ratio)

Penalty: $371 (10% of earnings portion)

Income tax owed: $3,709 × 22% = $816

Net proceeds: $10,813

This scenario shows why the penalty exists – it significantly reduces the net proceeds and encourages people to leave the money invested for long-term growth.

Long-term Growth Strategy

The accounts really shine when young adults resist the temptation to withdraw money and instead let it continue growing. Consider this comparison for a typical account:

Table 4: The True Cost of Early Withdrawals. How withdrawing money in your 20s dramatically impacts long-term wealth accumulation

The $20,000 withdrawn at age 25 ultimately costs over $300,000 in retirement wealth. This demonstrates why financial advisors emphasize the importance of leaving retirement accounts untouched whenever possible.

How Trump Accounts Compare to Other Savings Options

Understanding where Trump accounts fit in the landscape of children's savings options becomes much clearer when we examine them side by side. Let me walk you through a comprehensive comparison that highlights the strengths and limitations of each approach

Table 5: Complete Comparison of Children's Investment Account Options. Side-by-side analysis of key features across all major children's savings vehicles

Now let's explore how these differences play out in practice through detailed comparisons.

Trump Accounts vs. 529 College Savings Plans

529 plans remain the gold standard for college savings, and examining why helps us understand when Trump accounts might be more appropriate. The tax treatment tells much of the story. When you withdraw money from a 529 plan for qualified educational expenses, you pay zero taxes on the growth. This is an enormous advantage that compounds over time.

Consider the Martinez family, who want to save for their daughter Sofia's college education. They have $5,000 annually to invest and are comparing a Trump account to a 529 plan. After 18 years of contributions with 7% annual growth, both accounts would have approximately $180,000. However, when Sofia starts college, the tax implications differ dramatically.

529 Plan Scenario:

Total withdrawals for college: $180,000

Taxes owed: $0

Net amount available for college: $180,000

Trump Account Scenario:

Total withdrawals for college: $180,000

Estimated taxes on earnings portion (assuming 22% bracket): $19,800

Net amount available for college: $160,200

The 529 plan provides nearly $20,000 more in usable funds for educational expenses. Additionally, 529 plans allow much higher contribution limits. If the Martinez family could afford to save $15,000 annually instead of $5,000, they could do so with a 529 plan but would be limited to $5,000 with a Trump account.

However, Trump accounts offer advantages when college isn't the primary goal or when flexibility matters more than tax efficiency. Sofia might receive scholarships that cover most of her college costs, or she might choose a trade school rather than a traditional four-year college. In these scenarios, the Trump account's flexibility becomes valuable, while the 529 plan's unused funds face restrictions on how they can be used.

Trump Accounts vs. Custodial Roth IRAs

The comparison with custodial Roth IRAs reveals another set of trade-offs that depend heavily on your family's specific circumstances. Roth IRAs require children to have earned income during the year in order to contribute, while Trump accounts can be funded regardless of the child's income status.

Let's examine the Chen family's situation. They have a 16-year-old son, Kevin, who works part-time at a local restaurant earning $3,000 per year. They also have a 5-year-old daughter, Emma, who obviously has no earned income.

For Kevin (with earned income):

Custodial Roth IRA: Can contribute up to $3,000 (his earned income amount)

Trump Account: Can contribute up to $5,000

Roth IRA advantage: Withdrawals during retirement are completely tax-free

Trump Account advantage: Higher contribution limit, plus potential employer contributions

For Emma (no earned income):

Custodial Roth IRA: Cannot contribute anything

Trump Account: Can contribute up to $5,000 annually, plus she's eligible for the $1,000 government seed money

The long-term tax implications strongly favor the Roth IRA for retirement savings. Let's project Kevin's potential wealth at retirement if his parents contribute $3,000 annually to each account type for three years (ages 16-18), then he continues contributing on his own.

Table 6: Roth IRA vs. Trump Account Long-Term Tax Impact. Comparing retirement wealth and tax implications for identical contribution amounts

The Roth IRA's tax-free growth during retirement creates a substantial advantage that grows larger over time. However, the Trump account's accessibility for young adults and the government's seed money can offset some of this disadvantage, especially for families who value flexibility over maximum tax efficiency.

Trump Accounts vs. Regular Brokerage Accounts

Regular custodial brokerage accounts offer complete flexibility but miss out on the tax advantages and government contributions that make Trump accounts attractive. Let me illustrate this through the Williams family's experience.

The Williams family wants to save $5,000 annually for their daughter's future but aren't sure whether she'll attend college, start a business, or pursue other goals. They're comparing a Trump account to a regular brokerage account.

Regular Brokerage Account:

Investment flexibility: Can invest in individual stocks, bonds, REITs, international funds

Tax treatment: Annual taxes on dividends and capital gains distributions

Access: Money available anytime for any purpose

Growth drag: Annual taxes reduce compound growth over time

Trump Account:

Investment options: Limited to stock index funds

Tax treatment: No annual taxes, but ordinary income rates on withdrawals

Access: Locked until age 18, then IRA-style rules apply

Government boost: $1,000 initial contribution (if eligible)

Let's model both scenarios over 18 years with identical $5,000 annual contributions:

Table 7: Trump Account vs. Regular Brokerage Account Growth Comparison. How tax-deferred growth provides advantages over taxable investment accounts

The Trump account's tax-deferred growth provides a meaningful advantage, and this doesn't even include the potential $1,000 government contribution. However, the brokerage account offers immediate access to funds if needed for emergencies or opportunities before the child turns 18.

The Real Benefits: Beyond the Headlines

While the $1,000 government contribution gets the most attention, the true benefits of Trump accounts may be more subtle but equally important.

Financial Education and Engagement

Senator Ted Cruz, who originated the proposal, described the accounts as a way to help hook kids on investing and broader capitalist values, giving everyone "a stake" in American free enterprise. Having a growing investment account from birth could fundamentally change how children think about money, investing, and their relationship with the broader economy.

Accessibility for All Income Levels

Unlike many tax-advantaged accounts that primarily benefit high earners, Trump accounts are designed to be accessible regardless of family income. The government's $1,000 contribution provides a meaningful start for every eligible child, regardless of their parents' ability to contribute additional funds.

Simplified Investment Management

The mandate that funds be invested in low-cost index funds eliminates the possibility of poor investment choices that could devastate long-term returns. Many custodial accounts suffer from high fees or inappropriate investment selections; Trump accounts solve this problem through regulation.

Potential Drawbacks and Considerations

No financial product is perfect, and Trump accounts come with their own set of limitations that families should understand.

Limited Tax Advantages

Financial experts note that Trump accounts offer minimal tax benefits compared to alternatives like 529 plans or Roth IRAs. The tax-deferred growth is helpful, but the ordinary income tax treatment on withdrawals is less favorable than the tax-free treatment offered by Roth accounts or the capital gains treatment available in regular brokerage accounts.

Investment Restrictions

The requirement to invest in stock index funds means 100% equity exposure during the child's entire youth. This prevents the age-based rebalancing that many financial advisors recommend, where portfolios become more conservative as children approach college age.

Complexity and Confusion

Tax experts have noted that the rules governing Trump accounts are complicated and potentially confusing. The interaction between contribution limits, tax treatment, and withdrawal rules creates complexity that may discourage some families from participating.

Uncertain Implementation Details

Many important details about how Trump accounts will work in practice remain unclear and will require future IRS guidance. This uncertainty makes it difficult for families to plan comprehensive strategies around these accounts.

Strategic Considerations for Families

Given these characteristics, how should families think about incorporating Trump accounts into their broader financial planning? Let me walk you through several real-world scenarios that illustrate when these accounts make the most sense.

Scenario 1: The Young Professional Family (Starting to Save)

Meet the Thompson family: Jake is a software engineer earning $85,000, and Maria is a teacher earning $52,000. They have a 2-year-old daughter, Lily, and they're just beginning to think seriously about saving for her future. Currently, they can afford to save about $200 monthly ($2,400 annually) for Lily's needs.

Their Trump Account Strategy:

Contribute $2,400 annually to Lily's Trump account

Benefit from the $1,000 government seed money

Total 16-year contributions: $38,400 + $1,000 = $39,400

Projected Outcome (7% annual return):

Value when Lily turns 18: $69,442

If left untouched until Lily's retirement: $2,576,340

For the Thompson family, the Trump account provides an excellent foundation because it doesn't require choosing between college and retirement savings. The account's flexibility allows Lily to use the money for education, a home down payment, or long-term wealth building, depending on her path in life.

Scenario 2: The High-Earning Family (Multiple Account Strategy)

Now consider the Rodriguez family: Carlos is a cardiologist earning $350,000, and Linda is a financial advisor earning $125,000. They have three children ages 6, 9, and 12. They can afford to save significantly for their children's futures and want to maximize every available advantage.

Their Comprehensive Strategy:

529 Plans: $15,000 per child annually ($45,000 total)

Trump Accounts: $5,000 per child annually ($15,000 total)

Custodial Roth IRAs: For children with summer job income

Total annual savings for children: $60,000+

Why This Makes Sense: The Rodriguez family is already maximizing college savings through 529 plans, which offer superior tax treatment for educational expenses. However, they add Trump accounts as a retirement jumpstart for each child. This strategy acknowledges that their children might receive scholarships or choose less expensive education paths, leaving them with substantial unused 529 funds. The Trump accounts provide a parallel wealth-building track focused on long-term financial independence.

Table 8: Wealthy Family Multi-Account Strategy Results. How high-earning families can maximize different account types for comprehensive child financial planning

Scenario 3: The Business Owner Family (Employee Benefit Strategy)

Sarah owns a growing marketing agency with 25 employees. She's looking for creative ways to enhance her employee benefits package without dramatically increasing costs, while also maximizing benefits for her own two children.

Her Business Strategy:

Offers $2,000 per child Trump account contributions as an employee benefit

Average employee has 1.2 children = 30 total contributions

Annual business cost: $60,000

Tax deduction for business: $60,000

Net cost after tax savings (assuming 25% rate): $45,000

Employee Value Calculation: An employee with two young children receives $4,000 annually in tax-free benefits. Over 16 years, this represents $64,000 in contributions that could grow to over $140,000 by the time the children reach 18. This creates tremendous perceived value for a relatively modest business expense.

Sarah's Personal Strategy: For her own children, Sarah maximizes both the business contribution ($2,000 per child) and adds personal contributions ($3,000 per child) to reach the $5,000 limit. This allows her to optimize her tax situation while providing maximum benefits to her children.

Scenario 4: The Grandparent Strategy

Robert and Helen are retired grandparents with eight grandchildren ranging in age from newborn to 16. They want to leave a meaningful legacy but are concerned about gift tax implications and want to see their money make an immediate impact.

Their Approach:

Contribute $5,000 annually to each grandchild's Trump account

Annual total: $40,000

Stays well below annual gift tax exclusion limits ($18,000 per recipient in 2024)

Creates immediate, visible impact through growing account balances

Legacy Impact Calculation: If Robert and Helen contribute $5,000 annually for each grandchild until they turn 18, the results vary by the child's current age:

Table 9: Grandparent Legacy Strategy by Child's Current Age. How starting Trump account contributions at different ages affects final outcomes

This strategy allows the grandparents to see their grandchildren's accounts grow during their lifetime while creating substantial wealth transfer without complex trust structures or gift tax concerns.

Scenario 5: The Single Parent Strategy

Maria is a single mother working as a nurse, earning $68,000 annually. She has two children, ages 7 and 10, and struggles to save consistently due to the demands of single parenthood and everyday expenses.

Her Realistic Approach:

Focuses on the $1,000 government contribution (both children were born after 2025)

Contributes $100 monthly ($1,200 annually) when possible

Occasionally misses contributions during financially tight months

Why This Still Works: Even with inconsistent contributions, Maria's children benefit significantly:

Child 1 (age 7, 11 years until 18):

Government contribution: $1,000

Maria's contributions: $1,200 × 8 years (assuming she misses 3 years) = $9,600

Total contributions: $10,600

Projected value at age 18: $23,891

Child 2 (age 10, 8 years until 18):

Government contribution: $1,000

Maria's contributions: $1,200 × 6 years (assuming she misses 2 years) = $7,200

Total contributions: $8,200

Projected value at age 18: $16,847

Even with modest and inconsistent contributions, Maria creates meaningful financial foundations for her children that could grow into substantial retirement wealth if left untouched.

Economic experts have long advocated for "baby bonds" or similar programs as a way to introduce more Americans to investing and potentially address wealth inequality. Trump accounts represent the first large-scale implementation of this concept in American policy.

The program will cost the government approximately $17 billion over 10 years, a relatively modest investment that could have profound long-term effects on American attitudes toward investing and wealth building.

Some economists argue that more progressive versions of baby bonds – providing larger initial contributions to lower-income families – would be more effective at addressing wealth inequality. However, the universal nature of Trump accounts ensures broad political support and social acceptance.

Practical Next Steps

Now that we've explored how Trump accounts work and when they make sense, let me guide you through the specific actions you should consider taking based on your family's situation. Think of this as your roadmap for implementation.

Step-by-Step Action Plan by Family Type

The key to success with Trump accounts lies in understanding exactly which steps apply to your situation and in what order you should take them. Let me walk you through the decision-making process.

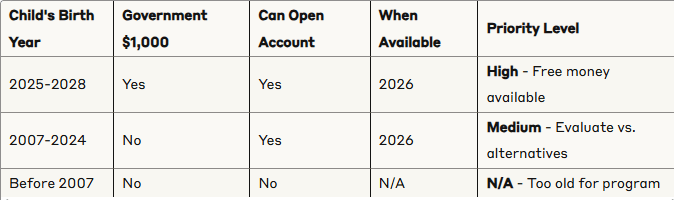

Step 1: Determine Your Children's Eligibility and Plan for 2026 Launch

First, identify which of your children qualify for different aspects of the program and understand the timeline for when you can actually open accounts:

Table 10: Child Eligibility and Account Availability Timeline. Determining which children qualify for benefits and when you can take action

Important: Even though the law was signed in 2025, you cannot open Trump accounts until financial institutions begin offering them in 2026. Use the remainder of 2025 to research and plan your strategy.

Step 2: Assess Your Current Savings Strategy

Before adding Trump accounts to your financial plan, take inventory of your existing children's savings approaches. This helps you understand where Trump accounts fit best.

Current Savings Assessment Worksheet:

Table 11: Family Financial Readiness Assessment. Key questions to determine how Trump accounts fit into your existing savings strategy

Step 3: Choose Your Contribution Strategy

Based on your assessment, select the approach that best fits your financial capacity and goals:

Conservative Strategy (Perfect for families just starting out):

Open accounts for children born 2025-2028 to claim $1,000 government money

Contribute $1,000-2,000 annually when budget allows

Focus on one child at a time if resources are limited

Expected outcome: $50,000-100,000 per child by age 18

Balanced Strategy (Ideal for middle-income families):

Maximize employer contributions if available ($2,500)

Add personal contributions to reach $4,000-5,000 total annually

Maintain separate 529 contributions for college-bound children

Expected outcome: $150,000-200,000 per child by age 18

Aggressive Strategy (Best for high-earning families):

Maximize Trump account contributions ($5,000 per child)

Coordinate with existing 529 and Roth IRA strategies

Consider business ownership benefits if applicable

Expected outcome: $200,000+ per child by age 18

Implementation Timeline and Milestones

Understanding when to take each action helps ensure you don't miss important opportunities or deadlines.

2025 (Preparation Year - Accounts Not Yet Available):

Research financial institutions that plan to offer Trump accounts

Calculate your optimal contribution amounts based on family budget

Discuss strategy with your spouse and financial advisor

If you own a business, design employee benefit structure for future implementation

Monitor IRS guidance releases for final implementation details

2026 (Launch Year - Accounts Become Available):

Open Trump accounts for eligible children as soon as institutions begin offering them

Set up automatic monthly contributions if desired ($417/month to reach $5,000 annual maximum)

Claim government $1,000 for children born in 2025 (retroactive) and 2026

Begin employer contribution programs if you're a business owner

Start making your first year's contributions

2027-2043 (Growth Years):

Make consistent annual contributions

Monitor account performance and adjust if needed

Claim government $1,000 for children born 2027-2028

Review strategy as children approach age 18

Beyond 2043 (Transition Years):

Help adult children understand their account options

Coordinate with college financing if applicable

Consider conversion strategies as they become clarified

Celebrate the long-term wealth you've created

Common Implementation Mistakes to Avoid

Learning from others' mistakes can save you time, money, and frustration. Here are the most important pitfalls to watch out for:

Mistake 1: Waiting Too Long to Start Many families delay opening accounts while they research or debate strategy. Remember, every month you wait is a month of potential compound growth lost.

Example Cost of Delay: Starting contributions in January vs. December of the same year:

Earlier start advantage: $420 more by age 18 (assuming 7% growth)

Multiply by number of children for total family impact

Mistake 2: Focusing Only on the $1,000 Government Contribution While the free money is attractive, the real value comes from consistent long-term contributions.

Comparison:

Government $1,000 only: $4,000 by age 18

Government $1,000 + $2,000 annually: $81,000 by age 18

The additional contributions create 20 times more value

Mistake 3: Not Coordinating with Other Savings Goals Trump accounts work best as part of a comprehensive financial plan, not as a replacement for other important savings.

Recommended Priority Order:

Emergency fund for family

Employer 401(k) match

High-interest debt elimination

529 contributions (if college is the primary goal)

Trump account contributions

Additional retirement savings

Mistake 4: Choosing the Wrong Financial Institution Since Trump accounts must be invested in index funds, fees become the primary differentiator between providers.

What to Compare:

Annual account fees

Expense ratios of available index funds

Customer service quality

Online platform usability

Educational resources provided

Special Considerations for Different Family Situations

Your family's unique circumstances might require modifications to the standard approach. Let me address some common special situations:

Divorced Parents: Either parent can contribute to a child's Trump account, and the contributions count toward their individual gift tax limits. Communication and coordination prevent over-contributions and maximize benefits.

Grandparents as Contributors: Grandparents can contribute directly to Trump accounts as gifts to grandchildren. This strategy works particularly well for estate planning purposes while staying below annual gift tax exclusion limits.

Special Needs Children: Trump accounts don't affect eligibility for government benefits the way some other assets might. However, consult with a special needs planning attorney to understand the full implications for your specific situation.

Military Families: Frequent moves and deployments can complicate account management. Choose financial institutions with strong online platforms and nationwide access to simplify administration.

Remember, the most important step is simply getting started. Trump accounts represent a significant opportunity to build long-term wealth for American children, but like all investment strategies, their success depends on consistent implementation over time. The families who benefit most will be those who start early, contribute regularly, and resist the temptation to withdraw funds before retirement age.

The Long-Term Vision

As President Trump stated when announcing the program, these accounts are designed to give children "the chance to experience the miracle of compounded growth and set them on a course for prosperity from the very beginning".

While Trump accounts aren't perfect and won't replace other important savings vehicles like 529 plans or Roth IRAs, they represent a meaningful step toward making investing accessible to all American families from birth. The program's success will ultimately be measured not just in dollars accumulated, but in whether it succeeds in creating a generation of Americans who understand and participate in long-term wealth building.

The accounts will become available starting in 2026, giving families time to understand the rules and plan how these accounts might fit into their broader financial strategies. This preparation period is valuable – use it to research providers, calculate contribution amounts, and coordinate with your existing savings goals. As implementation details become clearer over the next year, Trump accounts may prove to be either a valuable addition to the toolkit of children's savings options or simply a modest supplement to more effective alternatives.

What's certain is that any program that puts money in families' pockets and introduces children to the power of compound growth deserves serious consideration – especially when it comes with a $1,000 head start courtesy of the American taxpayer. The key is being ready to act when the accounts become available in 2026, so start your planning and research now.

Disclaimer

Important Legal and Financial Disclaimer

This blog post is provided for educational and informational purposes only and should not be construed as personalized financial, investment, tax, or legal advice. The information presented is based on current understanding of the "One Big Beautiful Bill" legislation as of August 2025, but implementation details, rules, and regulations may change as federal agencies issue additional guidance.

Key Important Notes:

Consult Professionals: Before making any financial decisions regarding Trump accounts or other investment vehicles, consult with qualified financial advisors, tax professionals, and estate planning attorneys who can provide advice tailored to your specific financial situation and goals.

Tax Implications Vary: Tax consequences discussed in this post are general in nature and may not apply to your specific situation. Tax laws are complex and subject to change. Individual circumstances, state tax laws, and future legislative changes can significantly impact outcomes.

Investment Risk: All investments carry risk, including the potential loss of principal. Past performance of market indexes does not guarantee future results. The projections and examples used in this post are hypothetical and for illustrative purposes only.

Legislation Subject to Change: While the "One Big Beautiful Bill" has been signed into law, implementation details are still being developed by federal agencies. Rules, procedures, and availability of Trump accounts may differ from what is described in this post.

Account Availability: Trump accounts are expected to become available in 2026, but the exact timing and participating financial institutions have not yet been finalized. Information about fees, investment options, and account features may change before accounts become available.

No Guarantee of Benefits: The government's $1,000 contribution and other benefits described are based on current law, which could be modified or repealed by future legislation.

The author and publisher assume no responsibility for errors or omissions in this content or for any losses that may arise from its use. Always verify current information with official government sources and qualified professionals before making financial decisions.